Bitcoin – Eine ausreifende Anlagethese

27 Januar 2021

Bitcoin gewinnt an Akzeptanz als Wertaufbewahrungsmittel und als Möglichkeit zur Diversifizierung von Investmentportfolios. Innovationen wie ein neues ETP sind ein wichtiges Instrument, um Investitionen praktikabler zu machen.

In der zweiten Jahreshälfte 2020 wurde Bitcoin vermehrt als eine Form von digitalem Gold anerkannt, eine Art digitaler Wertspeicher in einer von Unsicherheit geprägten Zeit. Zwischen Juli und Dezember hat sich der Preis mehr als verdreifacht, von 9.100 USD pro Bitcoin auf 29.000 USD (Stand: 31. Dezember 2020), wobei der größte Anstieg im Oktober und November stattfand. Der Grund? Eine wachsende institutionelle Akzeptanz und die zunehmende Zugänglichkeit der digitalen Währung.

Im August investierte MicroStrategy, ein börsennotiertes US-Unternehmen, sein gesamtes Barvermögen in Bitcoin. Dann, im Oktober, öffnete PayPal seine Plattform für den Kauf und Verkauf. Diese Ereignisse folgten auf die „Halbierung“ des Bitcoin im Mai, die planmäßige Reduzierung der Neuausgabe von Bitcoin, die etwa alle vier Jahre stattfindet und tendenziell zu Preissteigerungen führt.

Mit einem Preis, der sein Allzeithoch von 19.783 USD aus dem Jahr 2017 übertrifft, und einer größeren Akzeptanz im Finanz-Ökosystem, war 2020 ein bahnbrechendes Jahr für Bitcoin. Im Zuge dieser beiden Entwicklungen startete VanEck im November die VanEck Bitcoin ETN, die am Handelsplatz Xetra der Deutschen Börse gehandelt wird. Als eine der ersten voll besicherten Bitcoin Exchange Traded Notes (ETNs), die zudem von einem etablierten globalen Vermögensverwalter stammt, ist die Einführung ein wichtiger Schritt in der Weiterentwicklung der Kryptowährung, denn dadurch erhalten die Anleger Zugang zur Gesamtrendite von Bitcoin in einem bewährten und etablierten Format.

Seit der Gründung im Jahr 1955 hat sich VanEck den Ruf erworben, über die Finanzmärkte hinaus zu denken, um die Trends – einschließlich wirtschaftlicher, technologischer, politischer und gesellschaftlicher Entwicklungen – zu ermitteln, die unserer Meinung nach zu den besten Investitionsmöglichkeiten führen. Wir bieten zukunftsweisende, intelligent konzipierte Finanzprodukte, die Anlegern Zugang zu diesen Chancen verschaffen. VanEck war einer der ersten US-Vermögensverwalter, der Anlegern Zugang zu internationalen Märkten bot und frühzeitig das transformative Potenzial von Gold-Investments, Schwellenländern und ETFs erkannte. Heute verfügt das Unternehmen über ein verwaltetes Vermögen von 64 Mrd. USD.1

Bitcoin als potenzielles Wertaufbewahrungsmittel

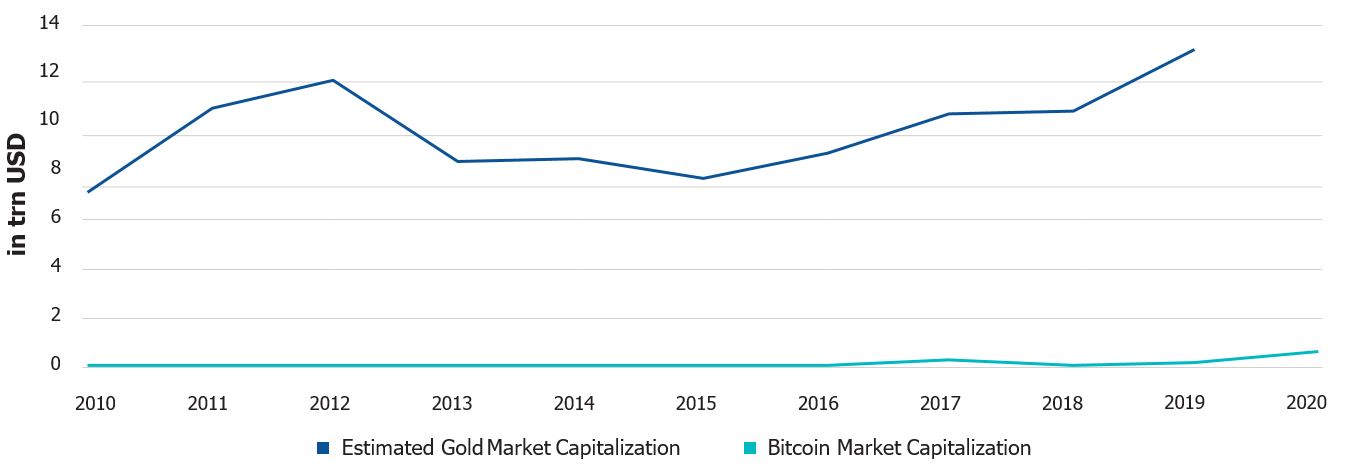

Die Ereignisse des Jahres 2020 knüpfen an die seit der Einführung von Bitcoin im Jahr 2009 an und deuten darauf hin, dass diese Kryptowährung zunehmend als eine digitale Form von Gold angesehen wird. Obwohl sein Umfang mit rund 540 Milliarden USD (Stand: 31. Dezember 2020) relativ klein bleibt, ist die Kapitalisierung von Bitcoin im Vergleich zu Gold gewachsen, das eine geschätzte Marktkapitalisierung von 12 Billionen USD aufweist. Dies entspricht etwa 5% der Marktkapitalisierung von Gold.

Es gibt zwei Arten von Wert – Eigenwert und Geldwert. Im Gegensatz zu Aktien oder Immobilien hat der Bitcoin nicht den Cashflow oder Nutzen, der dem Eigenwert zugrunde liegt. Aber wie Gold, Silber oder Kunst wird zunehmend sein Geldwert anerkannt – ein Wert, der aus einer Art kollektivem Glauben entsteht.

Je mehr Gesellschaften akzeptieren, dass ein Objekt einen Geldwert hat, desto wahrscheinlicher ist es, dass das Objekt in Zukunft auch wirklich einen Geldwert hat. Gesellschaften brauchen seit langem Geldwertspeicher, die flexibler sind als Sachwertspeicher.

Bitcoin Im Vergleich zu Gold-Marktkapitalisierung (in Billionen USD)

Quelle: Blockchain.info, World Gold Council, Bitcoin-Marktkapitalisierung zum 31. Dezember 2020, geschätzte Gold-Marktkapitalisierung zum 31. Dezember 2019.

Neue Formen von Geldwert werden nicht oft geschaffen. Kunst ist ein gutes Beispiel. Kunst hat vor allem in den letzten Jahrhunderten an Geldwert gewonnen. Ein vielleicht noch besseres Beispiel ist Gold. Gold erlangte einen Geldwert, weil es knapp, haltbar und relativ einfach zu Münzen und Barren zu formen ist. Ähnlich wie Gold hat der Bitcoin einen Geldwert, weil er knapp und langlebig und zudem ein Inhaberwert ist, was ihn in autoritären Regimen attraktiv macht.

Rolle in einem Anlageportfolio

So wie der Bitcoin wegen seines Geldwerts an Akzeptanz gewinnt, wird er auch zunehmend als Investment betrachtet. Es gibt mehrere Theorien, warum er ein attraktives Investment sein kann, nicht zuletzt wegen seines stetig steigenden Seltenheitswertes. Die Architektur des Bitcoin-Netzwerks bedeutet, dass seine heimische Währung (Bitcoin-Einheiten) in immer geringeren Mengen ausgegeben wird, bis das Angebot bei 21 Millionen liegt, woraufhin die Ausgabe gestoppt wird. Dieser steigende Stock-to-Flow-Ratio – die Menge eines Guts, das in den Beständen gehalten wird, geteilt durch die jährlich produzierte Menge – bringt den Bitcoin derzeit auf eine Stufe mit dem Stock-to-Flow-Ratio von Gold, einem Vermögenswert, der weithin als Absicherung gegen hohe Inflation angesehen wird. Sein Stock-to-Flow-Ratio wird bis zur nächsten Halbierung der Blockbeihilfe im Jahr 2024 weit über den von Gold steigen. Dagegen haben die Zentralbanken die Geldmenge in noch nie dagewesenem Ausmaß erhöht, um das Wachstum zu fördern. Gleichzeitig wird davon ausgegangen, dass die globale Verschuldung bis Ende 2020 auf 277 Bio. USD steigen wird, was 365% des BIP entspricht und um 20 Bio. USD höher ist als 2019.2

Quelle: VanEck.

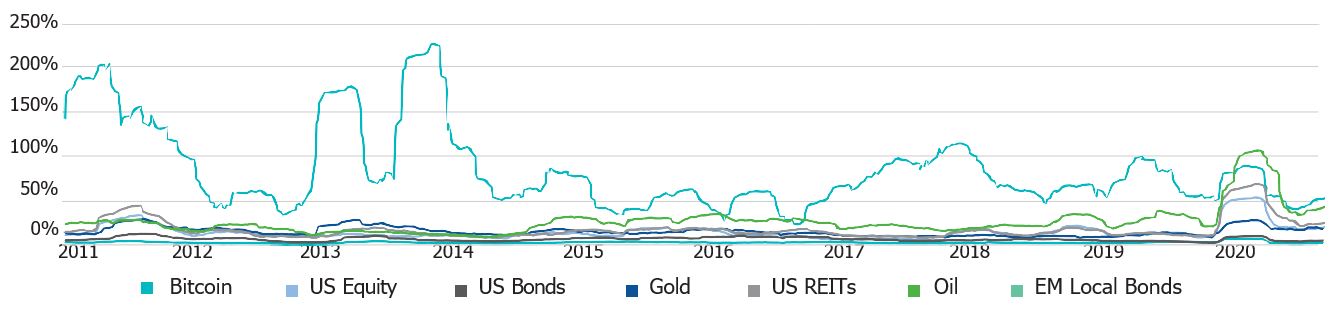

Der Bitcoin hat sich über die meisten langfristigen Zeiträume besser entwickelt als traditionelle Anlageklassen. In den fünf Jahren bis zum 30. September 2020 ist der digitale Anlagewert beispielsweise um annualisierte 122,1% gestiegen, gegenüber 14,1% für den S&P 500 Index für US-Aktien und 10,5% für weltweite Aktien. Selbst Gold hat sich mit einer annualisierten Rendite von 10,6% gemessen am Spot-Goldkurs schlechter entwickelt als der Bitcoin.

Darüber hinaus haben sich die Kurse des Bitcoin weitgehend unabhängig von großen Anlageklassen wie Aktien, Anleihen oder Gold bewegt. Man bezeichnet dies auch als geringe Korrelation.

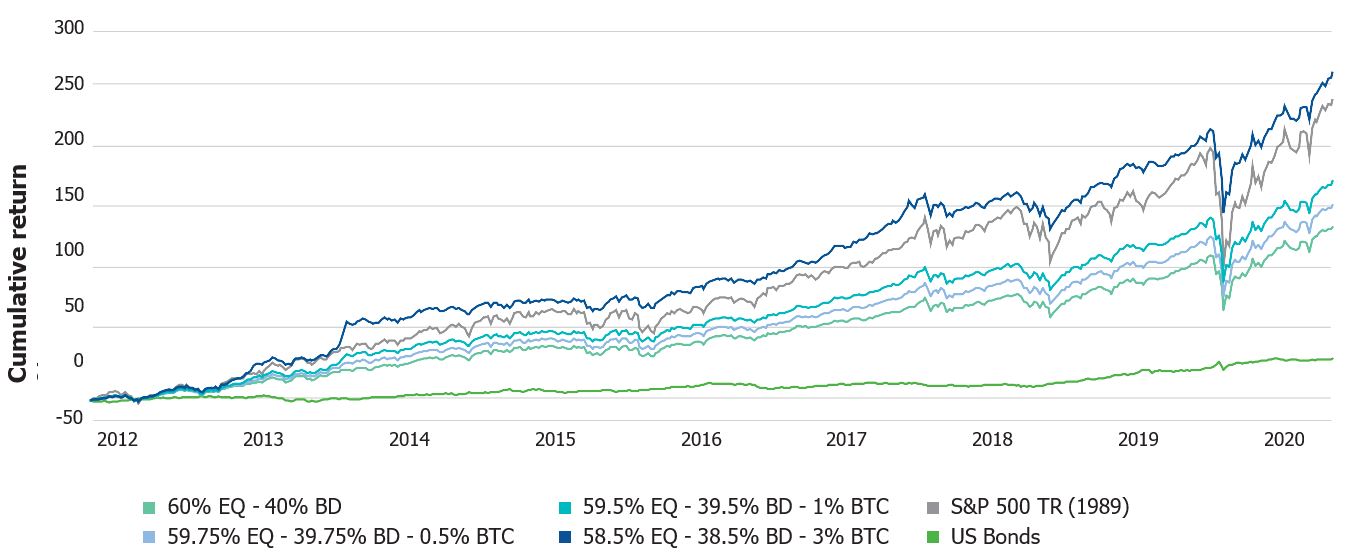

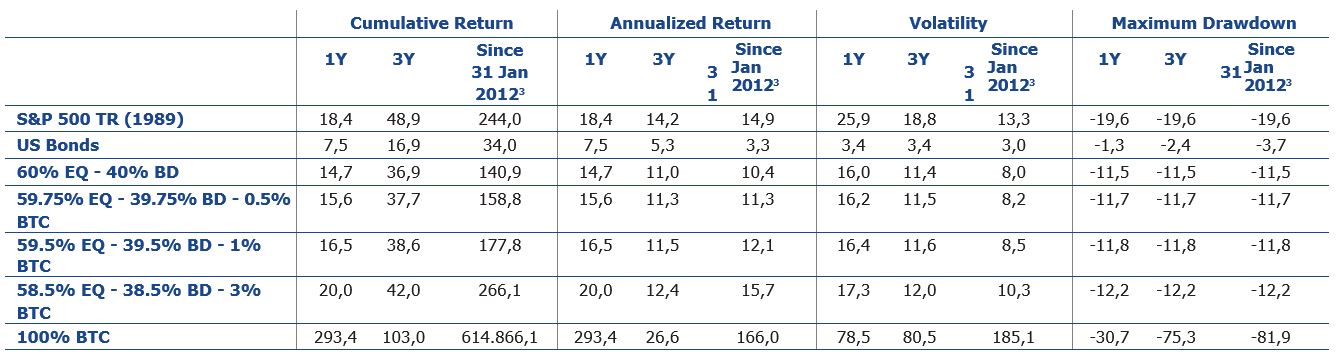

Diese Eigenschaft macht ihn als Mittel zur Diversifizierung eines breiten Anlageportfolios noch wertvoller. Angemerkt sei jedoch, dass in Zeiten äußerst hoher Stressphasen an den Märkten, wie z. B. in Krisen, die Korrelation des Bitcoin-Preises gegenüber anderen Anlageklassen zunimmt. All dies deutet darauf hin, dass eine geringe Allokation in Bitcoin die langfristige Performance eines diversifizierten Investmentportfolios, das typischerweise eine Allokation von 60% in Aktien und 40% in Anleihen aufweist, verbessern kann. Eine Allokation von 3% eines solchen Portfolios in Bitcoin würde zu einer Allokation von 58,5% in Aktien, 38,5% in Anleihen und eben 3% in der Kryptowährung führen. Über den Zeitraum von Anfang 2012 bis Ende September 2020 hätte eine solche Allokation eine annualisierte Rendite von 14,77% erzielt, im Vergleich zu 9,75% für das standardmäßige Portfolio von 60% Aktien und 40% Anleihen.

Erstaunlicherweise hätte eine Aufnahme des Bitcoin, obwohl er als hoch riskante Anlage gilt, in ein traditionelles Portfolio auch die Standardabweichung gesenkt.

Asymmetrische Renditeprofile (31. Januar 2012 bis 31. Dezember 2020)

Quelle: Morningstar. Datenstand: 31. Dezember 2020. Wertentwicklung gemessen in US-Dollar. Die Wertentwicklung in der Vergangenheit ist keine Garantie für künftige Ergebnisse.

Gleichwohl ist der Bitcoin nicht frei von Risiken. Das erste Risiko betrifft die Volatilität. Der Wertzuwachs wurde durch einige starke Kursverluste unterbrochen. Es muss jedoch angemerkt werden, dass der Bitcoin bis November weniger volatil war als viele Komponenten des S&P 500. Dann ist da noch die Sicherheit der Technologie. Obwohl der Bitcoin als sicher gilt, besteht immer die Möglichkeit, dass Handelsplattformen gehackt werden oder die Verschlüsselung des Bitcoin kompromittiert wird, insbesondere angesichts der Entwicklungen im Bereich der leistungsstarken Quantencomputer.

Beschleunigte Einführung

Vor diesem Hintergrund hat sich der Bitcoin stetig zu einem Teil des finanziellen Ökosystems entwickelt. Zuletzt entschied MicroStrategy, sein gesamtes Barvermögen von 425 Mio. USD in Bitcoin zu investieren, und PayPal entschied, den Kunden den direkten Handel mit Bitcoin zu ermöglichen.

Darüber hinaus beginnen die Regulierungsbehörden, den Bitcoin anzuerkennen. So hat zum Beispiel der US-Bundesstaat Colorado den Bitcoin von der staatlichen Wertpapierregulierung ausgenommen. In ähnlicher Weise war Liechtenstein eines der ersten Länder, das digitale Vermögenswerte regulierte, und Deutschland folgte diesem Beispiel mit einem Zusatz zum Kreditwesengesetz, der die Verwahrung von Kryptowährungen abdeckt. In der Europäischen Union wurde MiCa (Markets in Crypto Assets) entwickelt, um bei der Regulierung von Krypto-Werten und deren Dienstleistern zu helfen und so bis 2024 ein einheitliches Lizenzierungssystem in allen Mitgliedstaaten einzuführen. Zusätzlich treten etablierte Depotbanken und Broker in den Markt ein.

Die Bitcoin-Volatilität hat mit der Zeit abgenommen

Rollierende 90-Tage-Volatilität

Quelle: VanEck, Datenstand: 31. Dezember 2020. Die Wertentwicklung in der Vergangenheit ist keine Garantie für künftige Ergebnisse.

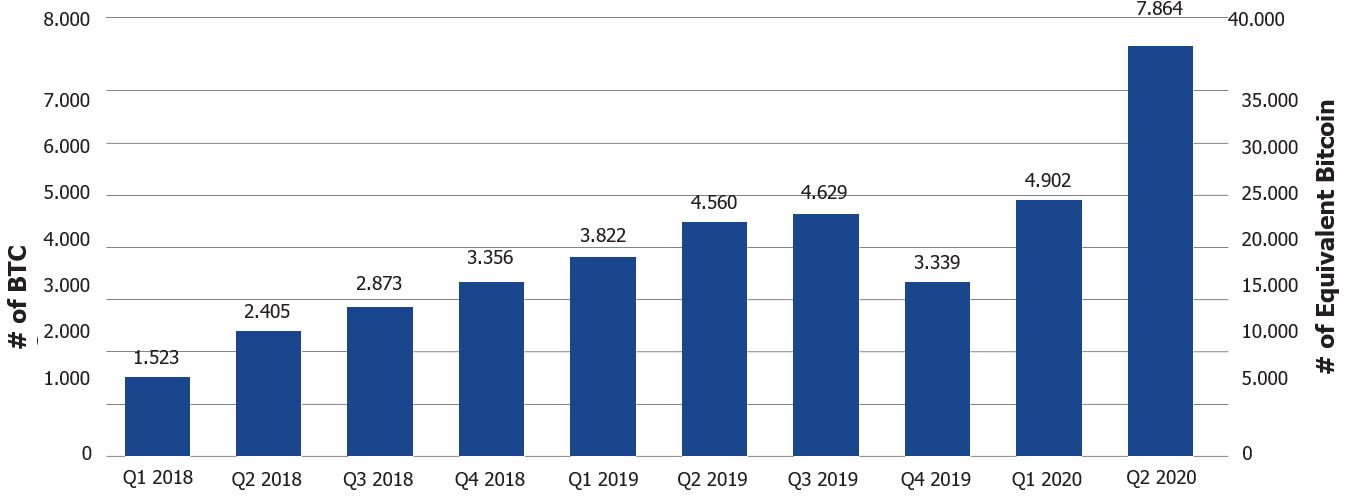

Das tägliche Handelsvolumen lag zuletzt bei 1,75 Mrd. USD.4 Die Anzahl der CME-Kontrakte erreichte gegen Ende des zweiten Quartals 2020 einen neuen Rekord mit 7.864 täglich offenen Positionen, was mehr als dem Doppelten des Werts am Ende des Jahres 2019 entsprach. Die Stiftungsfonds der Universitäten Harvard und Yale haben in Unternehmen und Risikokapitalfonds investiert, die von der fortschreitenden Verbreitung des Bitcoin profitieren werden, da die Einführung des Bitcoin als Geldwertspeicher allmählich erkannt wird.

CME Bitcoin-Futures – durchschnittliche tägliche offene Position

Quelle: CME Group. Datenstand: 30. Juni 2020.

Ganz bequem in den Bitcoin investieren

Trotzdem ist das Investieren in den Bitcoin unpraktisch geblieben. Der Kauf und vor allem die sichere Aufbewahrung von Bitcoin und anderen digitalen Vermögenswerten erfordern ein technisches Wissen, das man vom Durchschnittsnutzer nicht erwarten kann. Im Einklang mit unserer Verpflichtung, Finanzinnovationen zu unterstützen, hat VanEck ein physisch abgesichertes Bitcoin-ETP auf den Markt gebracht. Die am Handelsplatz Xetra der Deutschen Börse gehandelte VanEck Bitcoin ETN ist genauso einfach zu kaufen und zu verkaufen wie andere ETPs und erfordert nichts weiter als ein Brokerage-Konto. Anstatt Bitcoin an oft unregulierten Börsen zu kaufen und den Inhaberwert der Gefahr von Diebstahl, Hacks, Sicherheitslücken und vielem mehr auszusetzen, kann das Produkt an der regulierten Deutschen Börse gehandelt und von Banken und Brokern sicher verwahrt werden.

Um die Sicherheit zu fördern und die Standards von VanEck für transparente, kundenfreundliche Lösungen zu befolgen, ist das Produkt vollständig besichert und zu 100% durch Bitcoin gedeckt. Die Bitcoin werden im Cold-Storage eines regulierten Verwahrers aufbewahrt. Anstatt den privaten Schlüssel eines Bitcoin selbst zu sichern, können sich Anleger auf die bewährte technische Infrastruktur der Bank Frick & Co. AG verlassen, einem regulierten Finanzinstitut und regulierten Kryptoverwahrer nach Liechtensteiner Recht.

Durch die Replikation der Preis- und Renditeentwicklung des MVIS CryptoCompare Bitcoin VWAP Close Index, ist der ETP-Investor auch berechtigt, Renditen aus potenziellen „Hard-Forks“ zu erhalten – Änderungen am zugrunde liegenden Protokoll, die nicht vorwärtskompatibel sind und zu zwei Versionen des Netzwerks führen. Dies ist in der Vergangenheit unzählige Male passiert, und Investoren, die nur den Spotpreis von Bitcoin verfolgen, hätten diesen Teil der Rendite verpasst. Zwei der bekanntesten Hard-Forks von Bitcoin sind Bitcoin Cash und Bitcoin Gold. Der Bitcoin hat sich von einem kleinen Cypher-Punk-Experiment zum Beginn einer ganz neuen Anlageklasse entwickelt und dabei die Sichtweise der Welt auf expansive Geldpolitik und staatliche Eingriffe verändert. Dies geschieht zu einer Zeit, in der viele Anleger ihre Renditeerwartungen aus traditionellen Sparformen / Anlageklassen schwinden sehen, da die versteckte Inflation ihre Vermögensbasis langsam aufzehrt.

Der Bitcoin bietet eine sinnvolle Alternative zu diesen traditionellen Anlageklassen, indem er Investoren einen unkorrelierten Renditestrom bietet, der von einer zuverlässigen, perfekt vorhersehbaren, disinflationären Geldbasis unterstützt wird.

Erfahren Sie mehr über das Investieren in Bitcoin

1Stand der Daten: 30. September 2020.

2Global Debt Monitor: Attack of the Debt Tsunami; Institute of International Finance, November 2020.

3Auflegung des Index am 31. Januar 2012.

4Cryptocompare. Datenstand: 31. Dezember 2019.

Index Definitionen

Alle Indizes sind unverwaltet und beinhalten die Wiederanlage aller Erträge, spiegeln aber nicht die Zahlung von Transaktionskosten oder -aufwendungen wider, die typischerweise mit Portfolios digitaler Assets verbunden sind. Die Indizes wurden nur zur Veranschaulichung ausgewählt und sind keine Wertpapiere, in die investiert werden kann. Die Renditen tatsächlicher Konten, die in digitale Assets investieren, werden wahrscheinlich von der Wertentwicklung des jeweiligen entsprechenden Index abweichen. Darüber hinaus werden die Renditen der Konten aus einer Vielzahl von Gründen, einschließlich des Zeitpunkts und der individuellen Kontoziele und -beschränkungen, von der Wertentwicklung der Indizes abweichen. Dementsprechend kann nicht zugesichert werden, dass die Vorteile und das Risiko-Ertrags-Profil der dargestellten Indizes denen der tatsächlich verwalteten Konten ähnlich sind. Die Wertentwicklung wird nur für den angegebenen Zeitraum angezeigt.

S&P® 500 Index: Ein um den Streubesitz bereinigter, marktgewichteter Index von 500 führenden US-Unternehmen aus allen Marktsektoren. Der MVIS CryptoCompare Bitcoin VWAP Close Index misst die Wertentwicklung eines aus digitalen Vermögenswerten bestehenden Portfolios, das in Bitcoin investiert.

Alle aufgeführten S&P-Indizes sind Produkte von S&P Dow Jones Indices LLC und/oder seinen verbundenen Unternehmen, und Van Eck Associates Corporation hat für deren Nutzung eine Lizenz erhalten. Copyright © 2018 S&P Dow Jones Indices LLC, ein Unternehmensbereich von S&P Global, Inc., und/oder ihrer verbundenen Unternehmen. Alle Rechte vorbehalten. Die Weitergabe oder Vervielfältigung dieses Dokuments – ob auszugsweise oder vollständig – ist ohne die vorherige schriftliche Genehmigung von S&P Dow Jones Indices LLC verboten. Weitere Informationen zu den Indizes von S&P Dow Jones Indices LLC finden Sie unter www.spdji.com. S&P® ist eine eingetragene Marke von S&P Global und Dow Jones® ist eine eingetragene Marke von Dow Jones Trademark Holdings LLC. Weder S&P Dow Jones Indices LLC noch Dow Jones Trademark Holdings LLC und ihre jeweiligen verbundenen Unternehmen oder deren Drittlizenzgeber geben ausdrückliche oder stillschweigende Erklärungen oder Zusicherungen in Bezug auf die Fähigkeit eines Index, die Anlageklassen oder Marktsektoren, die er darstellen soll, präzise abzubilden. Weder S&P Dow Jones Indices LLC noch Dow Jones Trademark Holdings LLC und ihre jeweiligen verbundenen Unternehmen oder deren Drittlizenzgeber haften für Fehler, Auslassungen oder Unterbrechungen eines Index oder der darin enthaltenen Daten.

MV Index Solutions (MVIS®) entwickelt, überwacht und vermarktet die MVIS-Indizes, eine fokussierte Auswahl von reinen und investierbaren Indizes, die als Grundlage für Finanzprodukte dienen. Sie decken mehrere Anlageklassen ab, darunter Hard Assets und die internen Aktienmärkte sowie die Märkte für festverzinsliche Wertpapiere. MVIS ist das Indexgeschäft von VanEck, einer in den USA ansässigen Investmentmanagementfirma. Anlagen sind generell mit Risiken verbunden, die auch einen möglichen Verlust des eingesetzten Kapitals einschließen können. Wie bei allen Anlagestrategien gibt es keine Garantie dafür, dass die Anlageziele erreicht werden, und für die Investoren sind Verluste möglich. Diversifikation garantiert keinen Gewinn und auch keinen Schutz vor Verlusten bei rückläufigen Märkten. Die Wertentwicklung in der Vergangenheit ist keine Garantie für künftige Ergebnisse.

Wichtige Hinweise

Ausschließlich zu Informations- und/oder Werbezwecken.

Diese Informationen stammen von der VanEck (Europe) GmbH, Kreuznacher Straße 30, 60486 Frankfurt am Main. Sie sind nur dazu bestimmt, Anlegern allgemeine und vorläufige Informationen zu bieten, und sollten nicht als Anlage-, Rechts- oder Steuerberatung ausgelegt werden. Die VanEck (Europe) GmbH und ihre verbundenen und Tochterunternehmen (gemeinsam „VanEck“) übernehmen keine Haftung in Bezug auf Investitions-, Veräußerungs- oder Retentionsentscheidungen, die der Investor aufgrund dieser Informationen trifft. Die zum Ausdruck gebrachten Ansichten und Meinungen sind zum Veröffentlichungsdatum dieser Informationen aktuell und können sich mit den Marktbedingungen ändern. Bestimmte enthaltene Aussagen können Hochrechnungen, Prognosen und andere zukunftsorientierte Aussagen darstellen, die keine tatsächlichen Ergebnisse widerspiegeln. VanEck gibt weder ausdrückliche noch stillschweigende Zusicherungen oder Gewährleistungen in Bezug auf die Ratsamkeit einer Anlage in Wertpapiere oder digitale Vermögenswerte allgemein oder in das in diesen Informationen erwähnte Produkt oder die Fähigkeit des Basisindex zur Abbildung der Performance des maßgeblichen Marktes für digitale Vermögenswerte.

Der Basisindex ist das ausschließliche Eigentum der MV Index Solutions GmbH, welche die CryptoCompare Data Limited mit der Führung und Berechnung des Index beauftragt hat. Die CryptoCompare Data Limited verwendet größtmögliche Sorgfalt darauf, die korrekte Berechnung des Index sicherzustellen. Ungeachtet ihrer Verpflichtungen gegenüber der MV Index Solutions GmbH ist die CryptoCompare Data Limited nicht verpflichtet, Dritte auf Fehler im Index aufmerksam zu machen.

Anlagen sind generell mit Risiken verbunden, die auch mögliche finanzielle Verluste bis hin zum Verlust des gesamten eingesetzten Kapitals einschließen können. Sie müssen den Verkaufsprospekt und das Basisinformationsblatt lesen, bevor Sie eine Anlage tätigen. Ohne ausdrückliche schriftliche Genehmigung von VanEck ist es nicht gestattet, Inhalte dieser Publikation in jedweder Form zu vervielfältigen oder in einer anderen Publikation auf sie zu verweisen.

Anlagen in das Produkt sind mit einem Verlustrisiko verbunden, auch mit dem Risiko eines Totalverlusts.

© VanEck (Europe) GmbH.

Wichtige Hinweise

Ausschließlich zu Informations- und/oder Werbezwecken.

Diese Informationen stammen von VanEck (Europe) GmbH, die von der nach niederländischem Recht gegründeten und bei der niederländischen Finanzmarktaufsicht (AFM) registrierten Verwaltungsgesellschaft VanEck Asset Management B.V. zum Vertrieb der VanEck-Produkte in Europa bestellt wurde. Die VanEck (Europe) GmbH mit eingetragenem Sitz unter der Anschrift Kreuznacher Str. 30, 60486 Frankfurt, Deutschland, ist ein von der Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) beaufsichtigter Finanzdienstleister. Die Angaben sind nur dazu bestimmt, Anlegern allgemeine und vorläufige Informationen zu bieten, und sollten nicht als Anlage-, Rechts- oder Steuerberatung ausgelegt werden. Die VanEck (Europe) GmbH und ihre verbundenen und Tochterunternehmen (gemeinsam „VanEck“) übernehmen keine Haftung in Bezug auf Investitions-, Veräußerungs- oder Retentionsentscheidungen, die der Investor aufgrund dieser Informationen trifft. Die zum Ausdruck gebrachten Ansichten und Meinungen sind die des Autors bzw. der Autoren, aber nicht notwendigerweise die von VanEck. Die Meinungen sind zum Zeitpunkt der Veröffentlichung aktuell und können sich mit den Marktbedingungen ändern. Bestimmte enthaltene Aussagen können Hochrechnungen, Prognosen und andere zukunftsorientierte Aussagen darstellen, die keine tatsächlichen Ergebnisse widerspiegeln. Es wird angenommen, dass die von Dritten bereitgestellten Informationen zuverlässig sind. Diese Informationen wurden weder von unabhängigen Stellen auf ihre Korrektheit oder Vollständigkeit hin geprüft noch können sie garantiert werden. Alle genannten Indizes sind Kennzahlen für übliche Marktsektoren und Wertentwicklungen. Es ist nicht möglich, direkt in einen Index zu investieren.

Alle Angaben zur Wertentwicklung beziehen sich auf die Vergangenheit und sind keine Garantie für zukünftige Ergebnisse. Anlagen sind mit Risiken verbunden, die auch einen möglichen Verlust des eingesetzten Kapitals einschließen können. Sie müssen den Verkaufsprospekt und die KID lesen, bevor Sie eine Anlage tätigen.

Ohne ausdrückliche schriftliche Genehmigung von VanEck ist es nicht gestattet, Inhalte dieser Publikation in jedweder Form zu vervielfältigen oder in einer anderen Publikation auf sie zu verweisen.

© VanEck (Europe) GmbH

Verwandte Einblicke

Related Insights

10 Dezember 2023

10 Dezember 2023