Five Things to Know About High-Yield Municipal Bonds Now

February 19, 2020

Read Time 3 MIN

Will the tailwinds that drove strong municipal bond performance in 2019 continue through 2020? Last year, we saw the U.S. Federal Reserve (Fed) shift to a more dovish stance. Muni-specific factors also supported the market, including strong technicals, improving credit fundamentals and demand for tax exemption. As investors consider ways to gain exposure to the muni bond market, we believe the high yield space offers an attractive opportunity in the current environment. Here are five things we believe investors should know about high-yield munis in 2020.

1. High-yield municipal bonds have historically outperformed investment grade munis.

Credit spreads for high-yield munis have been stable, and higher coupons and longer duration have boosted performance. The Bloomberg Barclays Municipal High-Yield Index returned 12.65% in 2019.1 Rich valuations will make it difficult to repeat a year of double-digit gains in 2020, but spread narrowing may support positive returns. The benchmark is up 2.98% so far this year as of February 19, 2020.

2. Defaults remain low.

The total par value of first-time non-payments of interest or principal due was $3.6 billion in 2019.2This is just 0.09% of the $3.82 trillion market. Recent defaults have been generally from smaller healthcare sub-sectors such as nursing homes and continuing care retirement communities (CCRCs). These alone represented nearly three quarters of last year’s total.

3. Demand for munis continues, regardless of U.S. presidential election.

While it is too early to forecast the results of the election, a change in the White House may lead to changes in federal tax policy and impact the municipal market. The leading Democratic candidates support higher and/or new income taxes on high-income earners. Higher taxes historically support demand for tax-exempts, and even the possibility of higher taxes could contribute to positive fund flows. If Trump wins reelection, federal tax policies are likely to remain unchanged. No matter the outcome, we expect continued demand for municipal bonds.

4. The Fed is likely to hold interest rates steady.

In 2019, the Fed reversed its tightening stance and cut rates three times. Absent a significant economic shift, the Fed appears set to leave rates unchanged for the time being. As investors search for yield, we believe high-yield munis offer an opportunity to add extra income to their portfolios.5. Supply and demand imbalance appears likely to remain.

The total issuance of municipal bonds expanded by 21.9% in 2019.3 However, this was not nearly enough to meet the reinvestment demand generated by calls, coupon payments and maturing bonds, let alone the demand from mutual fund and ETF fund inflows, which totaled $93.6 billion last year.4 We expect a similar dynamic to play out in 2020. According to the SIFMA Municipal Issuance Survey, we may see a slight uptick in issuance this year, but demand has remained exceptionally strong, with funds reporting $9.7 billion of inflows as of January 22.

Constructive View for High-Yield Municipal Bonds

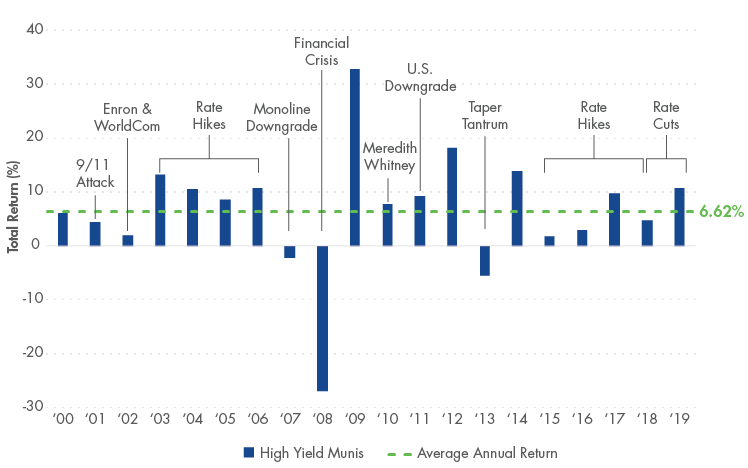

We remain constructive on high-yield municipal bonds in 2020 given the factors outlined above. Additionally, this asset class has a long history of low volatility, non-correlations, low default experience, attractive income and positive performance. While past performance is not reflective of future returns, we believe it is interesting to point out that over the past 20 years the Bloomberg Barclays High-Yield Municipal Bond Index has only been in the red in three years—all of which were headline driven rather than based on fundamentals.

Source: Bloomberg. Data as of12/31/2019. Past performance is no guarantee of future results. Indexes are unmanaged and are not securities in which an investment can be made. See index descriptions at the end of this presentation.

Learn more about VanEck’s suite of Municipal Bond ETFs and how they offer investors the ability to exercise control over their portfolio yield, duration and credit exposure at different points in the interest rate cycle.

Related Insights

Related Insights

April 02, 2024

February 21, 2024

February 02, 2024

IMPORTANT MUNI NATION® DISCLOSURE

1Source: Bloomberg. Data as of 12/31/2019.

2Source: Municipal Market Analytics, Inc. (MMA). Data as of 12/31/2019.

3Source: SIFMA

4Source: Lipper

This content is published in the United States for residents of specified countries. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this content. Nothing in this content should be considered a solicitation to buy or an offer to sell shares of any investment in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction, nor is it intended as investment, tax, financial, or legal advice. Investors should seek such professional advice for their particular situation and jurisdiction.

VanEck does not provide tax, legal or accounting advice. Investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service.

Please note this represents the views of the author and these views may change at any time and from time to time. MUNI NATION is not intended to be a forecast of future events, a guarantee of future results or investment advice. Current market conditions may not continue. Non-VanEck proprietary information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck. MUNI NATION is a trademark of Van Eck Associates Corporation.

Municipal bonds are subject to risks related to litigation, legislation, political change, conditions in underlying sectors or in local business communities and economies, bankruptcy or other changes in the issuer’s financial condition, and/or the discontinuance of taxes supporting the project or assets or the inability to collect revenues for the project or from the assets. Bonds and bond funds will decrease in value as interest rates rise. Additional risks include credit, interest rate, call, reinvestment, tax, market and lease obligation risk. High-yield municipal bonds are subject to greater risk of loss of income and principal than higher-rated securities, and are likely to be more sensitive to adverse economic changes or individual municipal developments than those of higher-rated securities. Municipal bonds may be less liquid than taxable bonds.

The income generated from some types of municipal bonds may be subject to state and local taxes as well as to federal taxes on capital gains and may also be subject to alternative minimum tax.

Diversification does not assure a profit or protect against loss.

Investing involves substantial risk and high volatility, including possible loss of principal. Bonds and bond funds will decrease in value as interest rates rise. An investor should consider the investment objective, risks, charges and expenses of a fund carefully before investing. To obtain a prospectus and summary prospectus, which contain this and other information, call 800.826.2333 or visit vaneck.com. Please read the prospectus and summary prospectus carefully before investing.Related Funds

IMPORTANT MUNI NATION® DISCLOSURE

1Source: Bloomberg. Data as of 12/31/2019.

2Source: Municipal Market Analytics, Inc. (MMA). Data as of 12/31/2019.

3Source: SIFMA

4Source: Lipper

This content is published in the United States for residents of specified countries. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this content. Nothing in this content should be considered a solicitation to buy or an offer to sell shares of any investment in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction, nor is it intended as investment, tax, financial, or legal advice. Investors should seek such professional advice for their particular situation and jurisdiction.

VanEck does not provide tax, legal or accounting advice. Investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service.

Please note this represents the views of the author and these views may change at any time and from time to time. MUNI NATION is not intended to be a forecast of future events, a guarantee of future results or investment advice. Current market conditions may not continue. Non-VanEck proprietary information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck. MUNI NATION is a trademark of Van Eck Associates Corporation.

Municipal bonds are subject to risks related to litigation, legislation, political change, conditions in underlying sectors or in local business communities and economies, bankruptcy or other changes in the issuer’s financial condition, and/or the discontinuance of taxes supporting the project or assets or the inability to collect revenues for the project or from the assets. Bonds and bond funds will decrease in value as interest rates rise. Additional risks include credit, interest rate, call, reinvestment, tax, market and lease obligation risk. High-yield municipal bonds are subject to greater risk of loss of income and principal than higher-rated securities, and are likely to be more sensitive to adverse economic changes or individual municipal developments than those of higher-rated securities. Municipal bonds may be less liquid than taxable bonds.

The income generated from some types of municipal bonds may be subject to state and local taxes as well as to federal taxes on capital gains and may also be subject to alternative minimum tax.

Diversification does not assure a profit or protect against loss.

Investing involves substantial risk and high volatility, including possible loss of principal. Bonds and bond funds will decrease in value as interest rates rise. An investor should consider the investment objective, risks, charges and expenses of a fund carefully before investing. To obtain a prospectus and summary prospectus, which contain this and other information, call 800.826.2333 or visit vaneck.com. Please read the prospectus and summary prospectus carefully before investing.