In Perspective: eSports and Video Gaming

23 July 2019

Over the last two years, media coverage of eSports, a form of competitive video gaming, has reached a fever pitch. News of sold-out stadiums, multi-million dollar franchise fees for professional teams and big-brand sponsorship deals have driven the eSports mania narrative. However, comparing eSports revenues to the broader video game industry can help keep things in perspective.

According to Newzoo, out of the $134 billion in revenue that the global video gaming industry generated in 2018, roughly $865 million was generated by eSports. In other words, the global video gaming industry generated around 154 times the revenue of the global eSports industry in 2018.

But what about all the front-page articles about the eSports boom? It’s easy to conflate the two industries, or at least to fail to draw a clear distinction between the two. At VanEck, we view the eSports industry as a sub-industry within the broader video game segment. Video game companies, in turn, are a convergence of technology and communication services. The video gaming and eSports industries encompass a wide range of companies, from video game publishers (Activision) to semiconductor companies (Nvidia) to media companies (HUYA).

Video game publishers and related hardware companies have been in business for decades, while the eSports business model is relatively young and in development. Although the top publisher companies generate significant video gaming revenues beyond eSports, they are among the biggest beneficiaries of eSports revenues.

Insert Coin to Play: Publishers Become League Operators

Over the past few years, video game publishers have invested millions of dollars in developing, launching and running professional eSports leagues. Previously, eSports leagues were run by independent third parties separate from the publishers who make the games. We believe the end result of this development is that video game publishers are now primed to gain the most from the eSports phenomenon.

Publishers own the rights to the games played in competition, as well as the broadcasting rights, which are sold to media and communication services companies (like Twitch and Facebook). According to Goldman Sachs, media rights are expected to grow from representing around 20% of all eSports revenues to 40% by 2022. This means that, after factoring in other revenue sources like sponsorship and game publisher fees, video game publishers are in a position to potentially own the majority of revenues coming from eSports.

Currently, revenues from eSports are still a relatively small part of publishers’ revenue streams and not typically broken out into a separate line item in financial statements. Activision Blizzard, which runs the highly successful Overwatch League and also owns Major League Gaming (MLG), reported $7.5 billion in consolidated net revenues in their 2018 annual report. Of that, only $607 million (8%) included revenues from its “Studios and Distribution business, as well as revenues from MLG and the Overwatch League.”

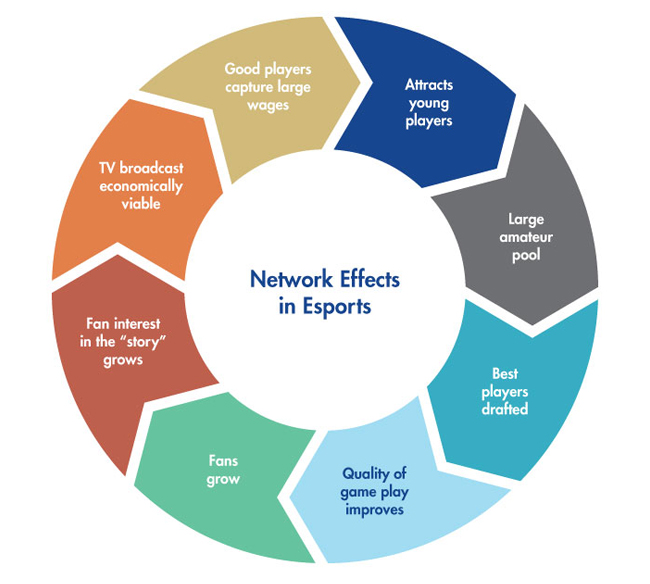

Power Up: Cultivating a Video Game Fan Base

A large eSports audience for a specific game typically equates to a large video game fan base. If publishers can build and maintain a popular international eSports leagues surrounding a hit title, then that should (in theory) sustain the popularity of the game itself among consumers, creating a positive feedback loop. This may lead to an expanded revenue cycle beyond a single transaction to purchase the game, to one with a much longer timeframe that includes additional in-game purchases and subscriptions. The effect is heightened even further under the new “game as service” model, where games are free to play while offering the option to buy add-ons and subscriptions to boost the user experience.

In a highly competitive entertainment landscape, publishers are actively looking for any edge to gain marketshare (and mindshare) among video game consumers and enthusiasts. eSports represent a unique and new way for companies to attract and retain loyal fans over a longer time period.

Source: Citi Research1

Investing in Video Gaming and eSports

Determining which games will become hits is difficult, and investors may wish to invest in a diversified basket of stocks. Such an approach may allow investors to express a view on the sector without having to know which specific stock will outperform over the future. The index methodology which guides VanEck Video Gaming and eSports UCITS ETF (ESPO) provides exposure to the largest, most successful companies in the video gaming and eSports industries.

Currently, the MVIS® Global Video Gaming and eSports Index is heavily tilted towards video game publishers (including the publicly traded companies that operate the largest eSports leagues) and semiconductor companies. As the eSports industry matures, smaller eSports names, such as streamers like HUYA and Modern Times Group, could grow to become a meaningful part of the Index. In the interim, the index captures the eSports phenomenon as part of the broader evolution of video gaming, creating awareness of the industry’s potential to reshape how people spend their time and entertainment dollars.

Click here to learn more about ESPO

1“Video Games: Cloud Invaders,” Citi Research

Important Disclosure

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

Related Insights

Related Insights

14 June 2023

06 September 2022

14 June 2023

06 September 2022