Spreads Boost EM High Yield Bonds Opportunity

09 September 2020

Like most credit oriented sectors, emerging markets high yield corporate bonds have rallied strongly over the past few months, after initially lagging U.S. high yield peers.1 With yields still over 7%, many income-seeking investors have taken notice, and we believe that an attractive opportunity remains in this asset class.

Compared with most other emerging markets debt sectors, high yield corporates have held up remarkably well. Although returns are still slightly negative year to date (-1% as of 31 July 2020), this represents significant outperformance versus high yield emerging markets sovereigns, which are down nearly 7% due to severe distress that several lower rated and financially weak countries have experienced following the onset of the pandemic.2 The default rate among emerging markets high yield sovereigns has already exceeded 16% year to date, compared with only about 2% among high yield emerging markets corporates, according to J.P. Morgan (as of June 9, 2020).

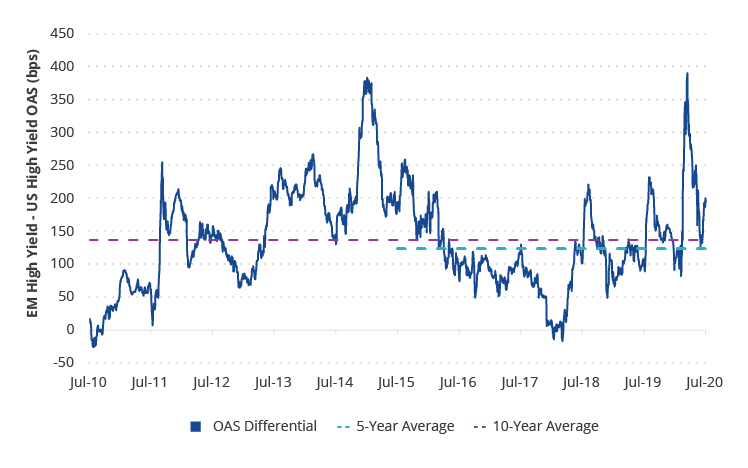

This relatively low default rate also compares favorably with U.S. high yield bonds, which have a default rate that is nearly twice as high. Despite the significant rally in spreads, emerging markets high yield remains attractive from a historical perspective. As of 31 July 2020, the asset class provided a spread pickup of nearly 200 basis points relative to U.S. high yield, nearly 60 basis points above the 10-year average.3 That spread is compensation for the perceived added risk of investing in emerging markets, and exists despite the fact that emerging markets high yield corporates have a higher BB allocation and lower CCC and below allocation than U.S. high yield.

Spread Pickup Above Historical Average

Source: ICE Data Indices. Data as of 31/7/2020. Emerging markets high yield corporate bonds represented by ICE BofA Diversified High Yield US Emerging Markets Corporate Plus Index. U.S. high yield corporate bonds represented by ICE BofA US High Yield Index.

In addition to the higher quality tilt, we believe there are several differences that may make emerging markets high yield an attractive part of a global high yield bond portfolio. To the extent the impressive recovery in China continues, we believe China issuers will likely remain among the largest contributors to performance in the index.4

The greater presence of quasi-sovereigns may also provide relative stability. For example, although exposure to energy issuers is approximately equal to the broad U.S. high yield market, emerging markets issuers within this sector have significantly outperformed.5 An increase in fallen angels, whether driven by weaker standalone fundamentals or sovereign downgrades, may also benefit returns for emerging markets corporates going forward. Including Pemex, there have been more than $80B of emerging markets fallen angels by market value in 2020, and we believe there is high potential for further downgrades over the next 12 months. Much as with developed market credit, fallen angels have been historically a source of excess return within the emerging markets high yield universe.

Several risks remain, including the ongoing tensions between the U.S. and China, the risks of a second wave and the impact of receding fiscal and monetary stimulus down the road. However, with the current spread pickup and potential catalysts for additional momentum, we believe emerging markets high yield corporates present an attractive opportunity.

1Emerging markets high yield corporate bonds represented by ICE BofA Diversified High Yield US Emerging Markets Corporate Plus Index. U.S. high yield corporate bonds represented by ICE BofA US High Yield Index.

2Source: ICE Data Indices.

3Source: ICE Data Indices.

4ICE BofA Diversified High Yield US Emerging Markets Corporate Plus Index

5Source: FactSet. Data as of 31/7/2020.

Important Disclosure

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.