Does Global Mining’s Golden Run Signal a Super-Cycle?

19 February 2021

A good sign of a reviving economy is the blistering run in the price of mining stocks since their Covid depths in March last year. Tracking the rising prices of the copper, iron ore, platinum and other metals, these global miners have recovered their losses and then kept on going.

Two of the world’s biggest miners have just confirmed their place as leaders of the recovery, giving shareholders a cash bonanza as miners enjoy their best conditions for a decade. I read with interest this week that BHP declared a record dividend and Glencore resumed pay-outs to investors after suspending them last year.

These are two of the world’s biggest miners. Along with others such as Anglo-American, Rio Tinto and Vale, they dominate production of the world’s metals. Speaking as he announced Glencore’s annual results last week, its CEO Ivan Glasenberg was bullish. Just as supply of metals is getting tighter, Chinese demand is booming, he said. If the US government now launches a major infrastructure investment programme that will ratchet up demand still further, he added, creating boom conditions1.

Metal prices reach multi-year highs

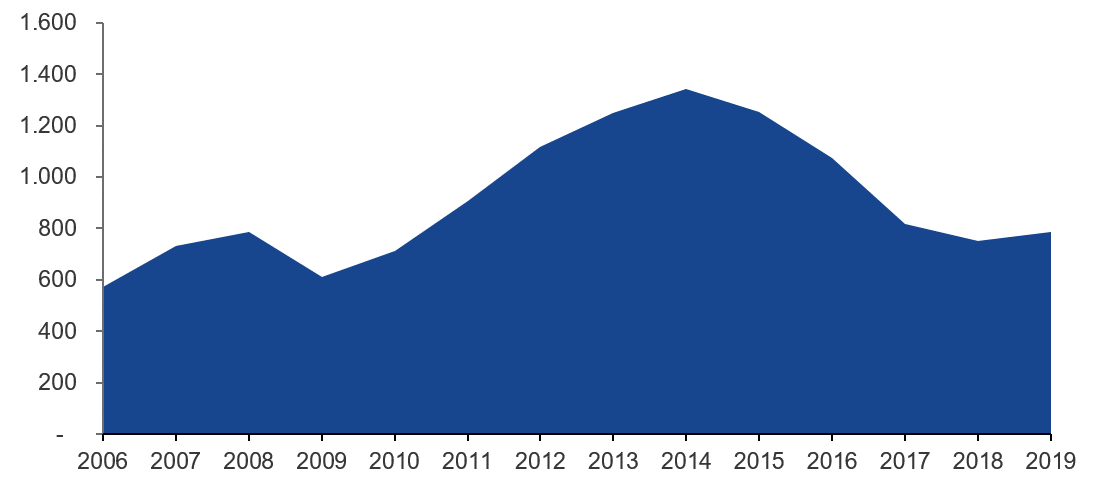

So, is this the beginning of a super-cycle, a prolonged period when rising demand outstrips supply? Typically, mining is a highly cyclical industry where capital expenditure goes through peaks and troughs, often leading to a shortage of supply just as demand picks up (figure 1). The last time this happened was in the 2000s, when a Chinese construction surge caught the industry unaware, leading to a super-cycle.

Figure 1 – Mining industry capex (EUR billion)

Source: McKinsey, Through-cycle investment in mining, 8 July 2020.

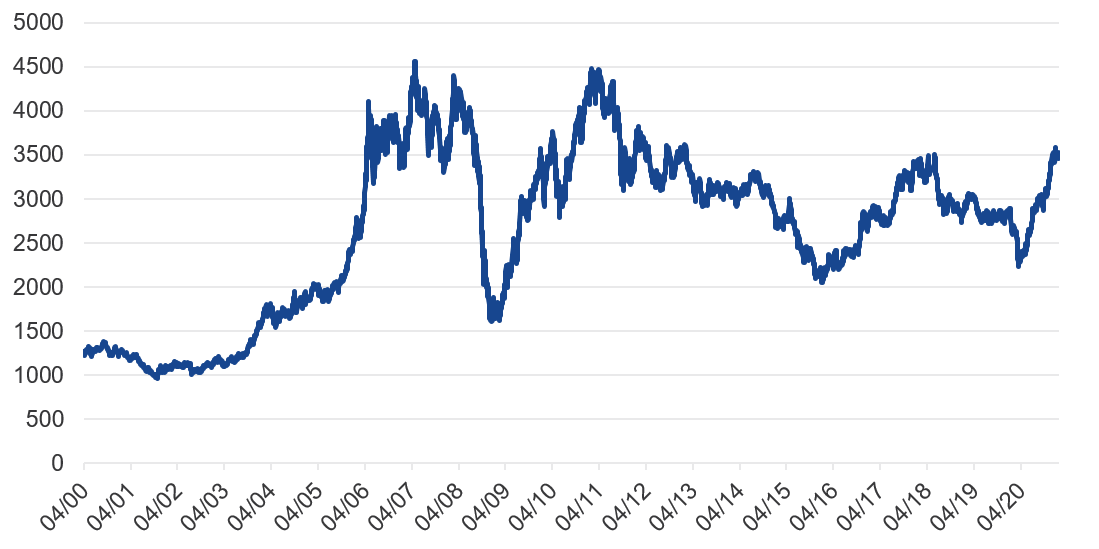

Certainly, metals prices are rocketing. The price of iron ore has soared almost 85% over the past year, reaching a nine-year high of US$175 a tonne in December before retrenching. Copper has risen 80% from its March lows to an eight-year high above US$8,400 a tonne.

Figure 2 - London Metal Exchange Index

Source: Bloomberg. Historical performance is not a reliable indicator for future performance. The London Metal Exchange LMEX Index is calculated once a day based on the closing prices of the six primary metals: copper, aluminum, lead, tin, zinc and nickel. It has a base value of 1000 starting in 1984.

Many think the coming transition to a low-carbon economy will stoke demand for metals such as steel and copper, used in wind turbines or wiring for solar panels and electric cars. The EU, UK and many other countries have pledged to remove carbon from their economies by 2050, with China doing so by 2060. Many of them have intermediate targets for 2030, meaning that the transition has to start immediately.

There will have to be a huge build out of wind power, solar panels, hydrogen electrolyser capacity, electric battery factories and so on. Within Europe alone, some 240-450 GW of offshore wind power is needed by 2050, according to the European Commission2. In a classic repeat of other commodity cycles, mining companies have not been investing in risky new exploration ventures so their supplies are limited.

A mining stock ETF

Many of the companies in the VanEck Global Mining UCITS ETF have reserves of metals that will be needed for this huge transition. The biggest of them, for instance, mine lithium, nickel and cobalt sulphate, all of which are used in batteries.

I can see that we will all be buying more metals soon, as we procure electric cars, heat pumps and solar panels. As a Dutchman, living below sea level in the Netherlands, I’m used to the idea of windmills limiting rising seas. The difference is that wooden Dutch windmills were historically used to pump sea water out, whereas today’s metal windmills should slow global warming and the sea’s rise in the first place!

In the meantime, anyone who shares the bullishness of Glencore’s Glasenberg can easily invest in a basket of the world’s leading mining companies through our mining ETF. This ETF offers exposure to mining stocks from around the globe, including developed and developing markets. These mining companies are the leading miners of gold, silver, copper, nickel, zinc, lithium and iron ore. They are the companies we will rely on as we turn to renewable power, electrifying the global economy.

Investors should consider risks before investing. Investing in mining companies entails risk related to natural resources, such as risk of depletion, risk of fluctuating prices and geopolitical risk. We do not intent to predict a super cycle. Market prices can also fall.

1Source: The Times.

2Source: European Commission.

Important Disclosure

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.