Ethereum Futures React to NFT “Jpeg Economy”

September 03, 2021

Read Time 8 MIN

VanEck assumes no liability for the content of any linked third-party site, and/or content hosted on external sites.

Key takeaways:

- NFT market annualizing at $43B; global art and antiques market is $50B.1 How can that be?

- Crypto is bullish for art prices, period.

- NFT gains may incentivize more ETH staking; ETH futures market growing strongly on CME in response?

- 2022 ETH estimates: the key levers.

The "jpeg economy" is now the size of small countries (well, Jordan & Turkmenistan), as #1 NFT platform OpenSea is reporting $3.55B in marketplace sales over the last 30 days.2 Maintaining that torrid pace would imply an annual GMV (gross merchandise value) of $43B for OpenSea, which now controls 98% of the NFT market.3 In comparison, the global art and antiques market totaled $50B in 2020. At first glance, one of these two markets may look mispriced to you. Dig into the details, however, and some more nuances emerge.

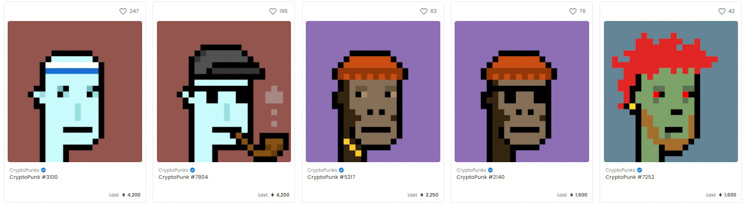

Still Value? Top 5 Cryptopunks NFTs Sold for an Average of $8M on OpenSea4; Top 5 Picassos Sold at Auction Average of $121M5

Source: OpenSea

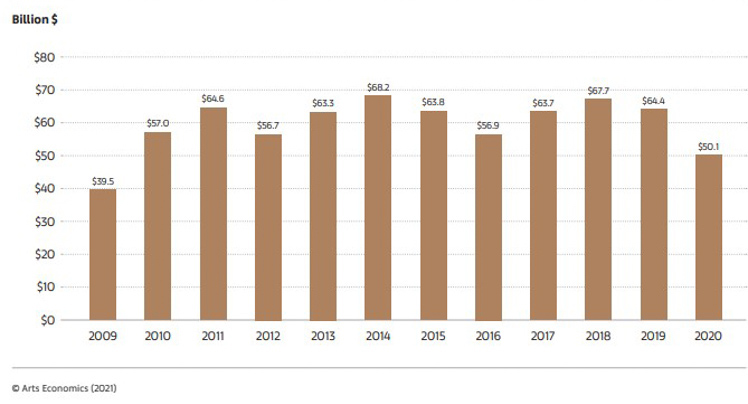

Sales in the Global Art Market (2009-2020)

Source: Art Economics & UBS

First, the velocity of digital assets has always been much higher than in traditional finance. Programmability, instant settlement, pseudonymity and 365/24/7 global trading are just a few of the features that encourage more frequent transactions. According to Goldman Sachs' research, the velocity of crypto is ~10x higher than that of stocks.6 Indeed, the OpenSea data reveal that 204k unique addresses have performed 2.28M NFT transactions in the last 30 days.7 That's an annualized "collectibles" turnover of 130x! Perhaps not sustainable to such a degree, but this is illustrative that advances in cryptography have created demand for transactions not previously economically rational.

Annualized Equity and Crypto Market Turnover

Source: Goldman Sachs, through 12/31/20

Second, and in support of the first point, although NFTs are theoretically "non-fungible", thanks to the power of DeFi, that is not entirely accurate. Most NFT creators earn royalties of between 2-5% every time their work is sold8, so their future income is tied to the art they create. Furthermore, DeFi and NFTs will soon converge, with leading lending protocols such as Aave (AAVE, mkt cap $6B) planning to accept NFTs as collateral in lending pools, according to Aave founder Stani Kulecov in a June twitter post. Fractional buying of NFTs, loans collateralized by NFTs, and event ticketing with special bonus features for NFT holders, as the USTA has piloted this year, will debut in coming quarters. As an example, the US Tennis Open's limited-edition NFT trading cards include "one-of-one" cards with specific benefits including backstage tours, playing in Arthur Ashe stadium, photo opps with the trophies, etc. FTX's CEO Sam Bankman-Fried, whose cryptocurrency exchange recently struck sponsorship deals with both the NBA (via the purchase of the Miami Heat Arena) and the MLB, said on a recent Twitter Spaces that he was working with the MLB on NFT ticketing. As those event and ticketing "cash" markets develop, a derivatives market that includes options to buy or sell access to certain events (and people) is likely to follow. Meanwhile, metaverse and gaming platforms such as Decentraland, Cryptovoxes and Nifty Island will use an "airdrops" or staking mechanisms to reward NFT holders with "free" digital currency or virtual goods in exchange for time spent.9 By producing a stream of cash flow, a portfolio of NFT assets will become fungible in DeFi.

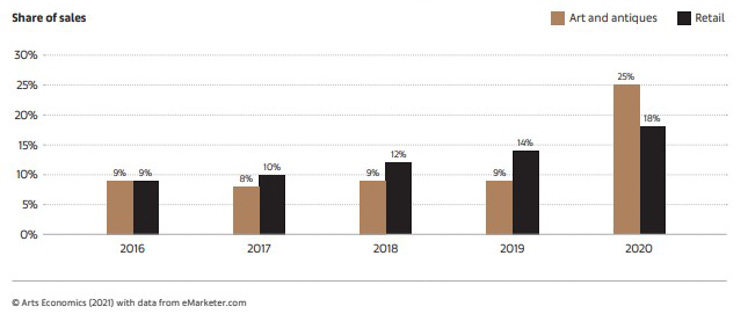

Lastly, in comparing the $50B art and collectibles markets to the $40B+ NFT market, we should note that velocity of traditional art is likely to rise because of the emergence of NFTs, even as the absurd 130% collectibles NFT turnover comes back to earth. Already, COVID-19 has turbocharged online sales of traditional art from 9% of total sales in 2019 to 25% in 2020. Investors are now more comfortable buying a work sight unseen. And with interest rates near zero and asset prices at high valuation, "some lenders say they're seeing more interest from wealthy art buyers who are willing to pledge paints as collateral in exchange for cash they can sink into other investments," according to a Bloomberg News report on August 13, which noted the yields on such packages of art-based loans at about 8%.10 In recent months, Bank of America has said its art-lending business grew by 15% year over year at the end of June, while Sotheby's financial services division said its loan book increase by almost 50% since 2018.11 With collectibles as a proof-of-concept, it seems likely that NFTs will permeate these real-world asset use cases, making it easier for investors to fractionalize, securitize, lend and trade art of every kind. More capital available to chase those 8% yields should be bullish for the asset class, new and old.

In a July interview on CNBC, the famed artist Damien Hirst, who has his own NFT project, said: “I’ve often thought about it like, in terms of the ‘Mona Lisa.’ Which would I rather own? The ‘Mona Lisa’ itself, with all the difficulties with looking at it because of the tourists and the bulletproof glass, or the merchandising possibilities? The T-shirts and the postcards and the earrings and the mugs.” For an extreme analogy of this insight, consider that Disney went public in 1957 as a collection of "real world art" that was packaged into bits and bytes for global consumers on a 60-year march to $330B in market cap.12 Disney keeps 100% of its IP. OpenSea takes 2.5%. OpenSea last raised capital in July at $1.5B.13

Share of Online Sales in the Art Market vs General Retail (2016-2020)

Source: Arts Economics

Disney Market Cap

Source: Bloomberg. Data as of 9/1/2021.

OpenSea "Mass Market" NFT Success Validates ETH Institutional Appeal

OpenSea's sudden dominance surprised many who predicted a more even playing field among NFT marketplace websites. That it leverages the Ethereum blockchain exclusively is a happy byproduct for ETH, which itself controls 72% of the DeFi market (though that number is falling with the rise of Solana and other chains better suited for even higher frequency trading).14 Given collectors' capital gains in NFT, there should be strong appetite to stake winnings in ETH (and crypto more generally) to avoid tax liabilities, however temporarily, as there are no tax liabilities until withdrawn to fiat. This tax arbitrage should also encourage more ETH-denominated purchases in the form of NFTs.

Total Locked in DeFi by Blockchain

Source: DefiLlama. Data as of 8/29/2021.

Meanwhile, unstaking ETH is a burdensome process that may take months. And as Ethereum fully transitions to proof-of-stake in 2022, an increasing proportion of ETH market participants may feel that friction. As such, it is interesting to note the much-improved liquidity in the CME's Ethereum futures contracts, whose average daily value traded now regularly exceeds $500M just six months since launch—a landmark that Bitcoin futures took two and half years to achieve.15 The futures' price spreads vs. spot have also improved considerably since the February 9 launch and now approach Bitcoin's, making the venue potentially a viable option for commercial players.

ETH vs BTC 30-day Average Value Traded

Source: CME, Bloomberg, VanEck. Data as of 8/31/2021.

Futures vs. Spot: Average Deviation. Since ETH CME Futures Inception (2/10/2021 - 8/24/2021)

Average spread between the CME CF Ether-Dollar Real Time Index and CME Futures at 4pm UK Time daily. Source: CME, Bloomberg, VanEck calculations, as of 8/24/2021.

The commercial market has thus acknowledged that ETH is a significant commodity, whose futures volumes exceed some assets with much longer histories, including assets that underlie existing futures-based ETFs such as the Breakwave Dry Bulk Shipping ETF (BDRY, mkt cap $81m, ADV $8M as of 9/1/2021). For context, lumber began trading on the CME in 1986, the Norwegian Krone in 2002, and the Polish Zloty in 2004.

Assorted Currency Futures: 30-Day Average Open Interest (7/21/2021 - 8/21/2021)

PLN = Polish Zloty, NOK = Norwegian Krone, RUB = Russian Ruble. Source: CME, Bloomberg, VanEck. Data as of 8/21/2021.

Assorted Commodity Futures: Total Open Interest (7/21/2021 - 8/21/2021)

Source: CME, Bloomberg, VanEck. Data as of 8/21/2021.

Lastly, we are in the midst of introducing our Ethereum estimates for 2022. Our initial estimates of $18B in protocol revenues for 2021, made three days after the market peak on May 12, are still within a few percentage points of the current run-rate of $17.3B, despite the 60% market correction from May to July.16 As usual, the lower gas prices17 attracted new applications that didn't make economic sense previously, and those applications (jpegs!) attracted users who are now in the money. With the 2022 transition to proof-of-stake, however, visibility gets much tougher. Getting next year right hinges on a few key inputs, including transaction growth, gas prices, amount staked, percent burned, and of course, for dollar investors, the ETH price. If you have questions or a view, feel free to get in touch: msigel@vaneck.com or on Twitter @matthew_sigel.

Related Insights

Related Insights

DISCLOSURES

1 ArtEconomics & UBS Research. https://d2u3kfwd92fzu7.cloudfront.net/The-Art-Market_2021.pdf

2 DappRadar https://dappradar.com/ethereum/marketplaces/opensea, World Bank https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?most_recent_value_desc=true.

3 The Block Research, 9/1/2021.

4 OpenSea website, https://opensea.io/collection/cryptopunks?collectionSlug=cryptopunks&search[sortAscending]=false&search[sortBy]=PRICE.

5 Artnews.com The Most Expensive Picassos to Sell at Auction – ARTnews.com

6 Goldman Sachs, through 12/31/20.

7 DappRadar https://dappradar.com/ethereum/marketplaces/opensea.

8 IntoTheBlock webinar, "The NFT Resurgence", 9/1/2021.

9 VanEck research.

10 "Fine art lending thrives, thanks to yield-hungry hedge funds," Bloomberg, 8/13/2021.

11 Ibid.

12 Bloomberg, as of 9/1/2021.

13 TechCrunch, 7/7/2021, https://techcrunch.com/2021/07/20/nft-market-opensea-hits-1-5-billion-valuation/.

14 DefiLlama, as of 8/29/2021.

15 CME, Bloomberg, VanEck. Data as of 8/31/2021

16 Bloomberg, TheBlock, VanEck research

17 “Gas” refers to the fee, denominated in ETH, required to successfully conduct a transaction on Ethereum.

VanEck assumes no liability for the content of any linked third-party site, and/or content hosted on external sites.

The information herein represents the opinion of the author(s), but not necessarily those of VanEck, and these opinions may change at any time and from time to time. Non-VanEck proprietary information contained herein has been obtained from sources believed to be reliable, but not guaranteed. VanEck does not guarantee the accuracy of third party data. Not intended to be a forecast of future events, a guarantee of future results or investment advice. Historical performance is not indicative of future results. Current data may differ from data quoted. Any graphs shown herein are for illustrative purposes only. Not a recommendation to buy or to sell any of the cryptocurrencies mentioned herein.

References to specific securities and their issuers or sectors are for illustrative purposes only.

Cryptocurrency is a digital representation of value that functions as a medium of exchange, a unit of account, or a store of value, but it does not have legal tender status. Cryptocurrencies are sometimes exchanged for U.S. dollars or other currencies around the world, but they are not generally backed or supported by any government or central bank. Their value is completely derived by market forces of supply and demand, and they are more volatile than traditional currencies. The value of cryptocurrency may be derived from the continued willingness of market participants to exchange fiat currency for cryptocurrency, which may result in the potential for permanent and total loss of value of a particular cryptocurrency should the market for that cryptocurrency disappear. Cryptocurrencies are not covered by either FDIC or SIPC insurance. Legislative and regulatory changes or actions at the state, federal, or international level may adversely affect the use, transfer, exchange, and value of cryptocurrency.

Investing in cryptocurrencies comes with a number of risks, including volatile market price swings or flash crashes, market manipulation, and cybersecurity risks. In addition, cryptocurrency markets and exchanges are not regulated with the same controls or customer protections available in equity, option, futures, or foreign exchange investing. There is no assurance that a person who accepts a cryptocurrency as payment today will continue to do so in the future.

Investors should conduct extensive research into the legitimacy of each individual cryptocurrency, including its platform, before investing. The features, functions, characteristics, operation, use and other properties of the specific cryptocurrency may be complex, technical, or difficult to understand or evaluate. The cryptocurrency may be vulnerable to attacks on the security, integrity or operation, including attacks using computing power sufficient to overwhelm the normal operation of the cryptocurrency’s blockchain or other underlying technology. Some cryptocurrency transactions will be deemed to be made when recorded on a public ledger, which is not necessarily the date or time that a transaction may have been initiated.

- Investors must have the financial ability, sophistication and willingness to bear the risks of an investment and a potential total loss of their entire investment in cryptocurrency.

- An investment in cryptocurrency is not suitable or desirable for all investors.

- Cryptocurrency has limited operating history or performance.

- Fees and expenses associated with a cryptocurrency investment may be substantial.

There may be risks posed by the lack of regulation for cryptocurrencies and any future regulatory developments could affect the viability and expansion of the use of cryptocurrencies. Investors should conduct extensive research before investing in cryptocurrencies.

Information provided by Van Eck is not intended to be, nor should it be construed as financial, tax or legal advice. It is not a recommendation to buy or sell an interest in cryptocurrencies.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

Related Funds

DISCLOSURES

1 ArtEconomics & UBS Research. https://d2u3kfwd92fzu7.cloudfront.net/The-Art-Market_2021.pdf

2 DappRadar https://dappradar.com/ethereum/marketplaces/opensea, World Bank https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?most_recent_value_desc=true.

3 The Block Research, 9/1/2021.

4 OpenSea website, https://opensea.io/collection/cryptopunks?collectionSlug=cryptopunks&search[sortAscending]=false&search[sortBy]=PRICE.

5 Artnews.com The Most Expensive Picassos to Sell at Auction – ARTnews.com

6 Goldman Sachs, through 12/31/20.

7 DappRadar https://dappradar.com/ethereum/marketplaces/opensea.

8 IntoTheBlock webinar, "The NFT Resurgence", 9/1/2021.

9 VanEck research.

10 "Fine art lending thrives, thanks to yield-hungry hedge funds," Bloomberg, 8/13/2021.

11 Ibid.

12 Bloomberg, as of 9/1/2021.

13 TechCrunch, 7/7/2021, https://techcrunch.com/2021/07/20/nft-market-opensea-hits-1-5-billion-valuation/.

14 DefiLlama, as of 8/29/2021.

15 CME, Bloomberg, VanEck. Data as of 8/31/2021

16 Bloomberg, TheBlock, VanEck research

17 “Gas” refers to the fee, denominated in ETH, required to successfully conduct a transaction on Ethereum.

VanEck assumes no liability for the content of any linked third-party site, and/or content hosted on external sites.

The information herein represents the opinion of the author(s), but not necessarily those of VanEck, and these opinions may change at any time and from time to time. Non-VanEck proprietary information contained herein has been obtained from sources believed to be reliable, but not guaranteed. VanEck does not guarantee the accuracy of third party data. Not intended to be a forecast of future events, a guarantee of future results or investment advice. Historical performance is not indicative of future results. Current data may differ from data quoted. Any graphs shown herein are for illustrative purposes only. Not a recommendation to buy or to sell any of the cryptocurrencies mentioned herein.

References to specific securities and their issuers or sectors are for illustrative purposes only.

Cryptocurrency is a digital representation of value that functions as a medium of exchange, a unit of account, or a store of value, but it does not have legal tender status. Cryptocurrencies are sometimes exchanged for U.S. dollars or other currencies around the world, but they are not generally backed or supported by any government or central bank. Their value is completely derived by market forces of supply and demand, and they are more volatile than traditional currencies. The value of cryptocurrency may be derived from the continued willingness of market participants to exchange fiat currency for cryptocurrency, which may result in the potential for permanent and total loss of value of a particular cryptocurrency should the market for that cryptocurrency disappear. Cryptocurrencies are not covered by either FDIC or SIPC insurance. Legislative and regulatory changes or actions at the state, federal, or international level may adversely affect the use, transfer, exchange, and value of cryptocurrency.

Investing in cryptocurrencies comes with a number of risks, including volatile market price swings or flash crashes, market manipulation, and cybersecurity risks. In addition, cryptocurrency markets and exchanges are not regulated with the same controls or customer protections available in equity, option, futures, or foreign exchange investing. There is no assurance that a person who accepts a cryptocurrency as payment today will continue to do so in the future.

Investors should conduct extensive research into the legitimacy of each individual cryptocurrency, including its platform, before investing. The features, functions, characteristics, operation, use and other properties of the specific cryptocurrency may be complex, technical, or difficult to understand or evaluate. The cryptocurrency may be vulnerable to attacks on the security, integrity or operation, including attacks using computing power sufficient to overwhelm the normal operation of the cryptocurrency’s blockchain or other underlying technology. Some cryptocurrency transactions will be deemed to be made when recorded on a public ledger, which is not necessarily the date or time that a transaction may have been initiated.

- Investors must have the financial ability, sophistication and willingness to bear the risks of an investment and a potential total loss of their entire investment in cryptocurrency.

- An investment in cryptocurrency is not suitable or desirable for all investors.

- Cryptocurrency has limited operating history or performance.

- Fees and expenses associated with a cryptocurrency investment may be substantial.

There may be risks posed by the lack of regulation for cryptocurrencies and any future regulatory developments could affect the viability and expansion of the use of cryptocurrencies. Investors should conduct extensive research before investing in cryptocurrencies.

Information provided by Van Eck is not intended to be, nor should it be construed as financial, tax or legal advice. It is not a recommendation to buy or sell an interest in cryptocurrencies.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.