Europe's Leading Role in Web3

15 July 2023

VanEck has been following the developments of the blockchain industry in Europe with great interest and optimism. Europe is not only a major player in the crypto space, but also a leader in many aspects. Something called the “MiCa effect” is set out to leave its mark permanently in the crypto industry (in a positive way). For your information, MiCA regulation (Markets in Crypto Assets Regulation for the European Union) was finalized and published in June 2023. Let me share with you some of the facts that support this claim:

Europe’s Leading Role in Crypto

- Europe is home to the highest number of Bitcoin and Ethereum nodes, which are the backbone of the decentralized networks that power these cryptocurrencies. According to Bitnodes, as of July 2023, Europe has over 2,728 Bitcoin nodes and 1,956 Ethereum nodes, accounting for 42.3% and 28.9% of the global total respectively (accounting only for publicly reachable nodes with a known geographical location).

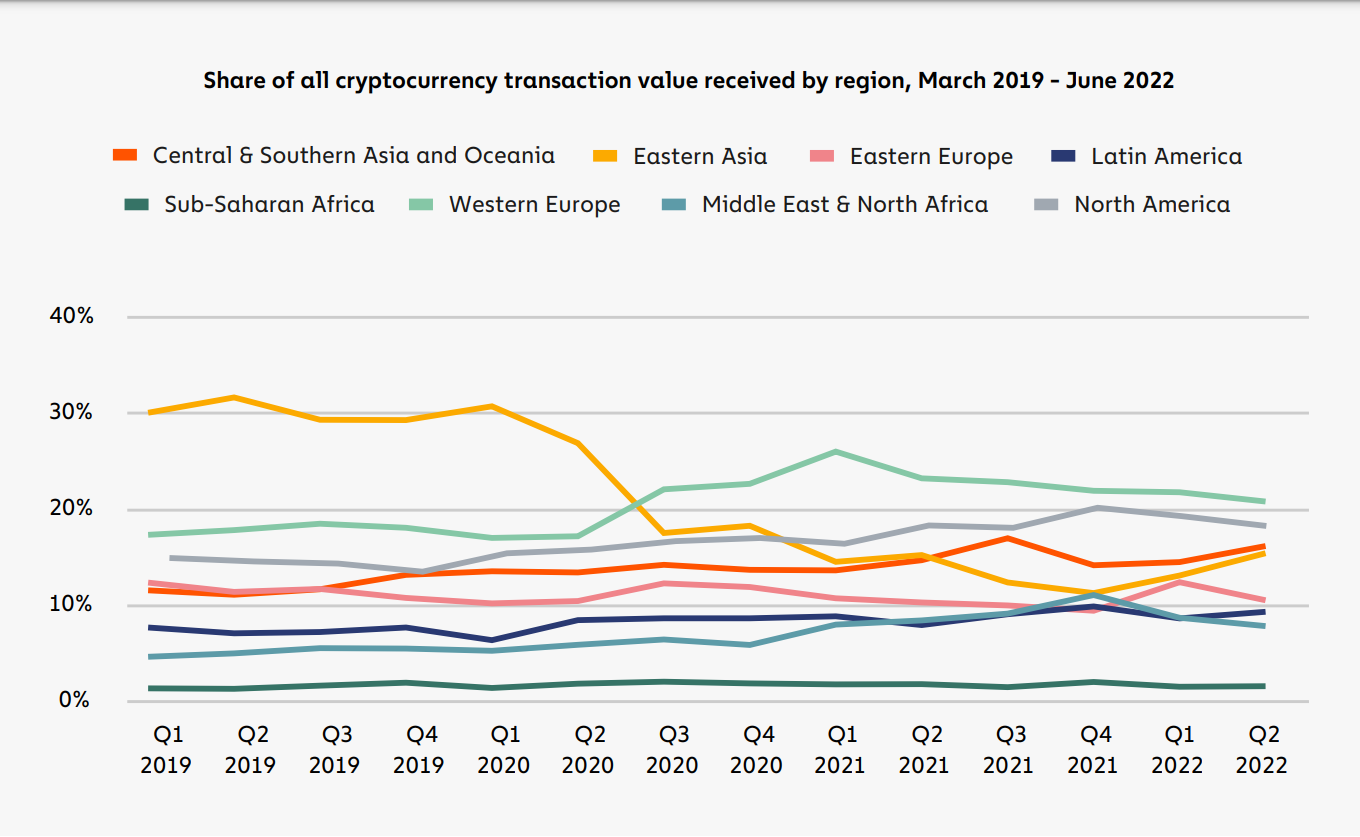

- Europe also has the largest absolute number and relative share of on-chain activity, which reflects the volume and diversity of transactions that take place on the blockchain. According to Chainalysis, in June 2022, Western Europe and Eastern Europe collectively have the largest share of on-chain transaction volume.

Source: Chainanalysis, data as of June 2022. Past performance is no indicator of future results

- Europe has the most comprehensive crypto-regulation globally, with the proposed Markets in Crypto-Assets (MiCA) regulation that aims to create a harmonized framework for crypto-assets across the European Union. MiCA will provide legal clarity and certainty for crypto-asset issuers, service providers and users, as well as enhance consumer protection and market integrity. MiCA will also foster innovation and competition by creating a level playing field for all market participants.

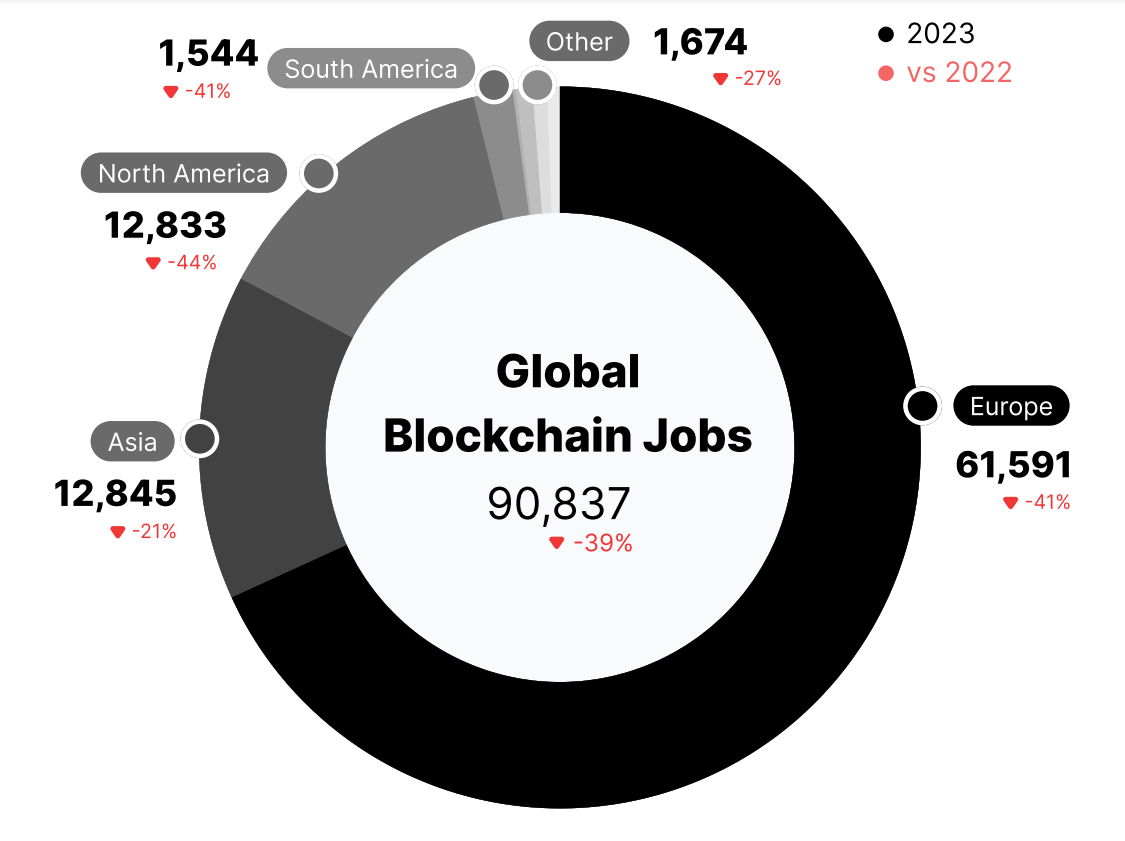

- Europe hosts two-thirds of global industry jobs, according to a report by Coincub. The report estimates that there are over 61,000 people employed in the crypto industry in Europe, compared to 12,845 in Asia and 12,833 in North America. While overall this is a decrease of -39% relative to 2022, we expect this to recover by the end of 2023 and the beginning of 2024 as regulation effects come into play. The report also ranks US, Germany and France as the top three countries in terms of crypto employment. According to a report of TrueUp, most open positions in June 2023 are from Binance, OKX and Token Metrics. Much like the decentralized nature of cryptocurrencies, over 25% are fully remote. As most jobs in crypto are engineering jobs, it also means that Europe likely is home to the largest number of blockchain developers.

Source: Coincub, data as of July 2023. Past performance is no indicator of future results

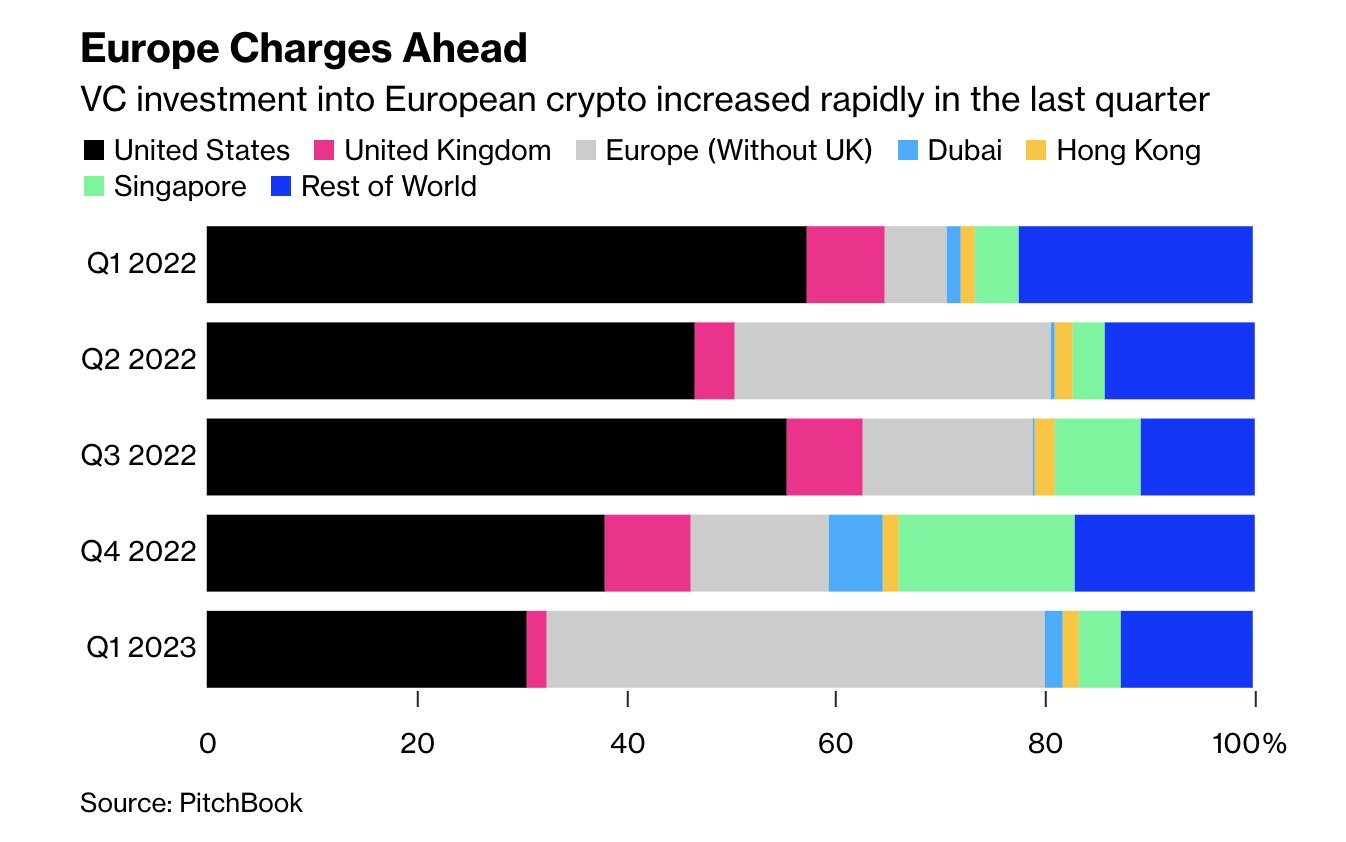

- Europe attracts 50% of venture-funded crypto projects globally, according to a study by Pitchbook. This figure is up approximately 7 times compares to Q1 2022. Other countries and regions have seen a significant decrease in crypto startup funding. This may be a leading indicator of a massive growth opportunity in Europe and for crypto in general.

Source: PitchBook, data as of April 2023. Past performance is no indicator of future results.

- Europe offers favourable tax regimes for crypto investors and entrepreneurs, according to a report by PwC. The report analyzes the tax treatment of crypto-assets in 29 jurisdictions around the world and ranks Malta, Portugal and Switzerland as the most attractive countries for crypto taxation in Europe. The report also notes that many European countries have issued clear and favourable tax guidance for crypto-assets, or have adopted a low or zero tax rate for certain types of crypto transactions. The reader should not perceive this as tax advice, please ask your tax advisor what taxation applies to your situation.

The MiCa Effect

These facts show that Europe is at the forefront of the blockchain revolution, and has the potential to leverage this technology to boost its economic growth and competitiveness. As a crypto specialist of a global asset manager, I am excited to be part of this journey and to help our clients navigate this fast-changing and promising landscape. For once, Europe has the chance to lead a major innovation. Our VanEck Crypto ETNs are well-positioned to benefit from the MiCa effect. Leading cryptocurrencies such as Bitcoin and Ethereum, or a basket such as Crypto Leaders or Smart Contract Leaders, is a great way to potentially benefit from the opportunity that this narrative provides. Please note that any historical performance mentioned in this article is no indicator of future results.

What is MiCAR?

MiCAR was published on the 9th of June, 2023. The first draft was created in 2018 following up after the bull run of Bitcoin in 2017. The main goal is to protect crypto users against unregulated virtual assets, fight money laundering and terrorist funding and protect the sovereignty of the Euro. It will make it significantly easier to operate in the EU and provide licensed services under MiCA’s harmonized European regulation. The regulation will apply in all EU member states as of 30 June 2024 for Asset Referencing Tokens (ARTs) and E-Money Tokens (EMTs) and 30th of December 2024 for Crypto Asset Service Providers (CASPs)

Important Information

We publish this newsletter to inform and educate about recent market developments and technological updates, not to give any recommendation for certain products or projects. The selection of articles should therefore not be understood as financial advice or recommendation for any specific product and/or digital asset. We may occasionally include analysis of past market, network performance expectations and/or on-chain performance. Historical performance is not indicative for future returns.

ETN Disclaimer

Important information

For informational and advertising purposes only.

This information originates from VanEck (Europe) GmbH, Kreuznacher Straße 30, 60486 Frankfurt am Main. It is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice. VanEck (Europe) GmbH and its associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. Views and opinions expressed are current as of the date of this information and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. VanEck makes no representation or warranty, express or implied regarding the advisability of investing in securities or digital assets generally or in the product mentioned in this information (the “Product”) or the ability of the underlying Index to track the performance of the relevant digital assets market.

The underlying Index is the exclusive property of MarketVector Indexes GmbH, which has contracted with CryptoCompare Data Limited to maintain and calculate the Index. CryptoCompare Data Limited uses its best efforts to ensure that the Index is calculated correctly. Irrespective of its obligations towards the MarketVector Indexes GmbH, CryptoCompare Data Limited has no obligation to point out errors in the Index to third parties.

Investing is subject to risk, including the possible loss of principal up to the entire invested amount and the extreme volatility that ETNs experience. You must read the prospectus and KID before investing, in order to fully understand the potential risks and rewards associated with the decision to invest in the Product. The approved Prospectus is available at www.vaneck.com. Please note that the approval of the prospectus should not be understood as an endorsement of the Products offered or admitted to trading on a regulated market.

Performance quoted represents past performance, which is no guarantee of future results and which may be lower or higher than current performance.

Current performance may be lower or higher than average annual returns shown. Performance shows 12 month performance to the most recent Quarter end for each of the last 5yrs where available. E.g. '1st year' shows the most recent of these 12-month periods and '2nd year' shows the previous 12 month period and so on. Performance data is displayed in Base Currency terms, with net income reinvested, net of fees. Brokerage or transaction fees will apply. Investment return and the principal value of an investment will fluctuate. Notes may be worth more or less than their original cost when redeemed.

Index returns are not ETN returns and do not reflect any management fees or brokerage expenses. An index’s performance is not illustrative of the ETN’s performance. Investors cannot invest directly in the Index. Indices are not securities in which investments can be made.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH

Important Disclosure

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.