A New Era and Renewed Relevance for Global Mining

September 25, 2020

Read Time 3 MIN

Having been so recently annealed in the “fire” of COVID-19, we believe the global metals and mining sector is now entering a nearly unprecedented new era. A period in which a tenacious focus on operational efficiency and optimal capital management is leading to improved returns, conservative balance sheets, strong free cash flow generation and increasing returns of capital directly to shareholders—via both dividends (ordinary and special) and share repurchase programs.

The commodity price swoons of 2012-2015 for metals created an existential crisis. These forced massive restructuring, dramatic strategic redirection and right-sizing and, in many cases, major changes in both company boards and management teams.

In delivering returns both on and of capital (rather than just volume growth in production), this new era has the potential to return these natural resource companies to their former relevance—both in the broader market and to generalist investors, not only in terms of leading free cash flow and dividend yield, but also per-share growth.

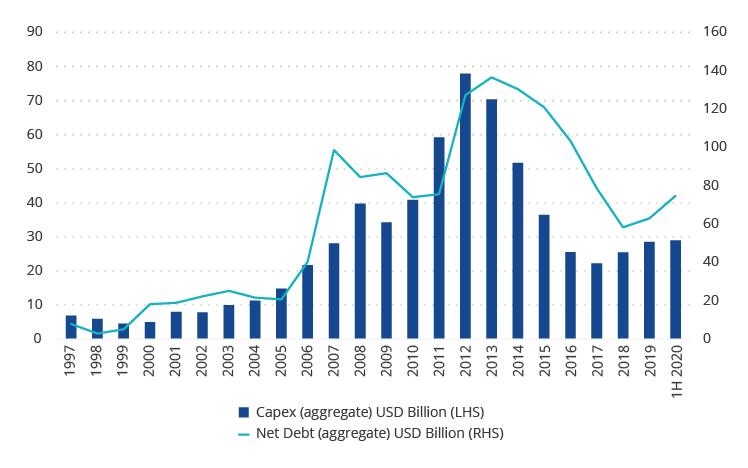

Dramatic Reductions in Capital Expenditure (Capex)

Metals and mining companies have undergone (and some, still, are currently undergoing) massive, transformative change. This can perhaps be illustrated no better than by looking at the significant reductions in capex that these companies have undertaken over the past several years. Back in 2012, such reductions would have been unimaginable, especially in the mining world.

For 2012, the aggregate capex of the “Big Six” diversified mining companies (BHP, Rio Tinto, Glencore, Vale, Teck Resources and Anglo American) stood at approximately $78B. By 2019 this figure had fallen nearly 64% and stood at just over $28B. By the middle of 2020, the projected capex for the full year stood at just under $29B.

Capital Expenditure and Net Debt: Diversified Miners

Source: VanEck. Data for: BHP, Rio Tinto, Glencore, Vale, Teck Resources and Anglo American

From an aggregate figure for net debt of over $127B in 2012, at the end of 2019, the Big Six had, together, reduced this figure by nearly 51% to just under $63B. (By the middle of 2020, however, it had risen somewhat to close to $75B.)

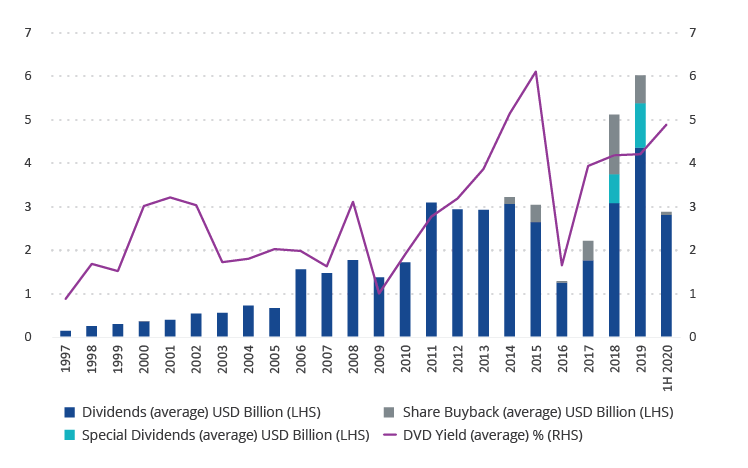

Stronger Returns

The intensified focus of companies on delivering stronger returns is best exemplified by the significant increases in free cash flow yields and, in turn, dividend yields and share repurchases.

We believe that capital will, increasingly, be returned to shareholders by way of dividends and share buybacks. We also believe that this is set to continue and remains a fundamental catalyst to unlock value.

Capital Return: Diversified Miners

Source: VanEck. Data for: BHP, Rio Tinto, Glencore, Vale, Teck Resources and Anglo American

This is well illustrated with just a couple of examples. In 2019, BHP Billiton increased the dividends (ordinary and special) it paid out by approximately 217% from $5.2B in 2018 to $16.6B. It also bought back $188M (2018: $171M) of shares, an increase of 10%.

Likewise, in 2019, Rio Tinto paid out $11.3B in dividends (2018: $9.4B), an increase of over 20%, and still bought back $1.2B of shares (2018: $6.0B), making its total return of capital to shareholders in 2019 $12.6B (2018: 15.3B).

Many companies are currently throwing off huge amounts of cash and will, we believe, increasingly return this cash to shareholders by way of dividends and/or share buybacks. At 4.88% at the end of June 2020, the Big Six global mining companies’ average dividend yield1 compared very favorably with a current dividend yield figure of 1.93%2 for the S&P® 5003 for the previous 12 months.

Looking Forward

We strongly believe that the free cash flow being generated by companies in the global metals and mining sector will be allocated to fund dividends and share buybacks and will be sustained for many years to come. As these companies committed themselves to cleaning up their balances sheets and espousing discipline, so, too, are managements now confirming their commitment to returning capital to shareholders, which we believe they will.

Benefiting, perhaps, from the example set by the gold mining sector, these mining companies, too, are proving themselves, now, not only to be well run, but also as having robust, stable and successful business models—the basis, we believe, of any sound investment. The result is that, while certainly not needing commodities prices to improve (the companies are already generating significant cash from current operations), any rises will just increase cash flow further.

To a broader investor base faced with the prospect of global interest rates remaining low and/or negative, we also believe this could, potentially, by very attractive.

Follow Us

DISCLOSURES

1 Investopedia: “The dividend yield–displayed as a percentage–is the amount of money a company pays shareholders for owning a share of its stock divided by its current stock price.”

2 Cormac Economic Research. Data point: June 28, 2020.

3 S&P 500® Index consists of 500 widely held common stocks, covering four broad sectors (industrials, utilities, financial and transportation).

Please note that the information herein represents the opinion of the author, but not necessarily those of VanEck, and this opinion may change at any time and from time to time. Non-VanEck proprietary information contained herein has been obtained from sources believed to be reliable, but not guaranteed. Not intended to be a forecast of future events, a guarantee of future results or investment advice. Historical performance is not indicative of future results. Current data may differ from data quoted. Any graphs shown herein are for illustrative purposes only. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

Please note that Van Eck Securities Corporation (an affiliated broker-dealer of Van Eck Associates Corporation) offers investments products that invest in the securities included in this commentary.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

Related Funds

DISCLOSURES

1 Investopedia: “The dividend yield–displayed as a percentage–is the amount of money a company pays shareholders for owning a share of its stock divided by its current stock price.”

2 Cormac Economic Research. Data point: June 28, 2020.

3 S&P 500® Index consists of 500 widely held common stocks, covering four broad sectors (industrials, utilities, financial and transportation).

Please note that the information herein represents the opinion of the author, but not necessarily those of VanEck, and this opinion may change at any time and from time to time. Non-VanEck proprietary information contained herein has been obtained from sources believed to be reliable, but not guaranteed. Not intended to be a forecast of future events, a guarantee of future results or investment advice. Historical performance is not indicative of future results. Current data may differ from data quoted. Any graphs shown herein are for illustrative purposes only. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

Please note that Van Eck Securities Corporation (an affiliated broker-dealer of Van Eck Associates Corporation) offers investments products that invest in the securities included in this commentary.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.