Fallen Angels – The Smarter High Yield Investment

03 September 2019

For some time now, action on the bond market has been characterised by a desperate search for returns, especially in the euro area. Here, the European Central Bank (ECB) has pushed down interest rates to levels not previously thought possible, and kept them there. A sharp and swift turnaround in which the ECB is prompted to raise its policy rate is regarded as highly unlikely. In fact, signs of economic weakness, triggered, for instance, by the trade dispute between the United States and China, are likely to mean the central banks will tend towards continuing with their expansionary monetary policy. The market is currently anticipating that the ECB will further depress interest rates by re-starting alternative stimulus measures from September onwards.

Companies around the world have taken advantage of long-lasting low interest rates to issue debt on attractive terms. In the last economic upswing this worked very well. Most corporates were able to increase their debt cheaply because they had good credit ratings. The market for US corporate bonds alone has now expanded to around USD 6,000 billion. Of these, bonds with an outstanding notional of USD 800 billion have a rating of BBB-, the lowest investment grade rating. Meanwhile, only USD 120 billion worth of these US corporate bonds are on negative watch with the rating agencies. These bonds in particular are in danger of slipping into high yield i.e. non- investment-grade territory.

When bonds suffer this fate, they are referred to as “fallen angels”. This exclusion from bond heaven usually goes hand in hand with declining bond prices. Most institutional bond investors are not willing or not permitted by the regulators to hold high yield bonds. Past experience has shown that the price does not decline after the downgrade has taken place. Instead, the market is very good at anticipating a rating change. During this adjustment phase, a change of ownership takes place. The new bond holders are increasingly investors specialising in the high yield segment.

Price distortions mostly remain a temporary phenomenon

Usually the price of downgraded bonds recovers in the months thereafter, as soon as the change of ownership is complete. Added to this is a rating advantage: Fallen Angel ratings are skewed towards the BB segment compared to a lower average rating for the board high yield market. This rating advantage acts as a buffer against the high yield segment as a whole.

Sometimes bonds even make it back into the investment grade universe at a later stage. In addition, the companies are usually well-established with tried and tested business models and have experience in typical business and sector cycles. Examples are UK retailer Tesco and Telecom Italia.

By aiming for the long term, the threat of a wave of downgrades can be significantly mitigated. In the past it has actually proven advantageous for fallen angel investors if the number of available bonds increases. In fact, unlike the investment grade segment, the market for high yield paper has hardly grown in recent years.

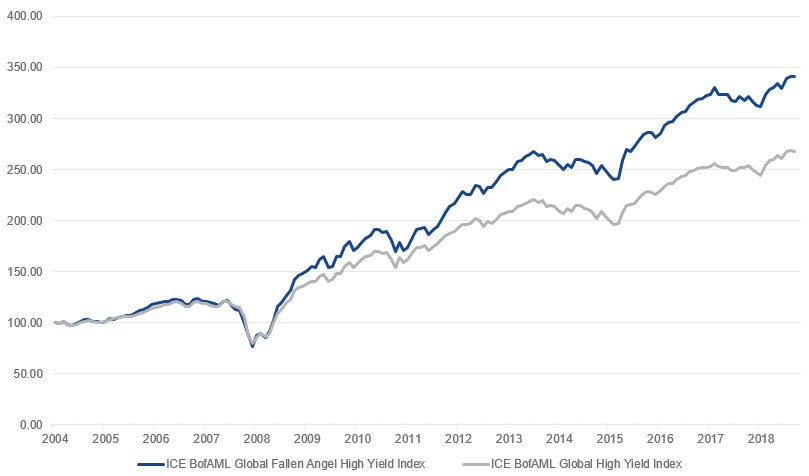

Fallen angels have advantages in terms of performance and rating

How can investors best cover this segment? It is noticeable that an investment in the high yield universe as a whole does not offer the prospect of additional value. Instead, over the medium and long term the fallen agents sub-segment has structurally outperformed the global high yield market.

Indeed, a comparison of the relevant indices from ICE BofAML over a period of 15 years demonstrates a clear advantage. The ICE BofAML Global Fallen Angel High Yield Index significantly outperformed the Global High Yield Index from the same provider. The bonds represented in both indices are generally denominated in one of four currencies – Euro, US dollars, Canadian dollars or British pounds.

Performance since 31 December 2004

Source: ICE Data Indices, LLC. Data as at: 31 August 2019.

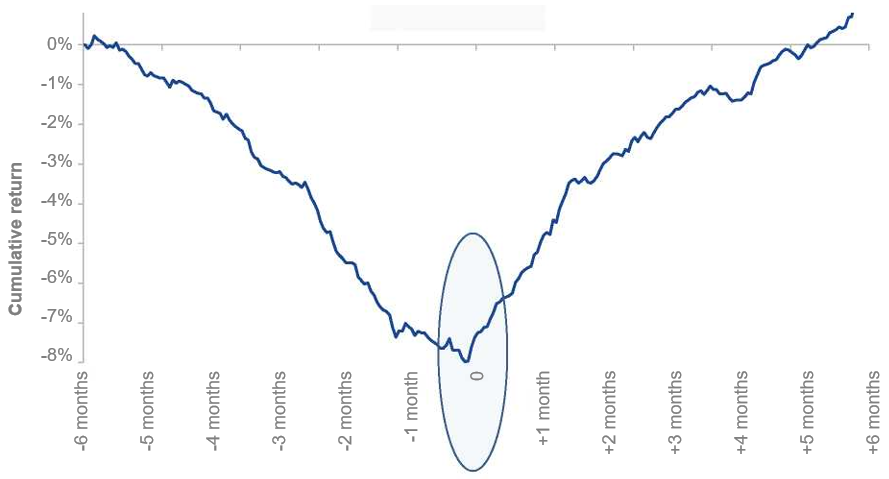

The background: fallen angel bonds usually slip below their fair value well before an impending rating downgrade. This collapse in price is usually over after about six months. After around another six months, the bonds have regained their fair value. Investors that buy in this period when the ownership structure is shifting can share in this recovery.

Average annualised cumulative return on fallen angel bonds from six months before to six months after their inclusion in the index

Source: FactSet. Data as at: 31 December 2017. The data are based on bonds in the ICE BofAML Global Fallen Angel High Yield Index that were downgraded to high yield and included in the index in 2004 or later.

A further advantage is the better average rating compared to the broad high yield market: in the past it has often been the BB rating segment that has outperformed here. In addition, fallen angels can be regarded as a lagging indicator. With these bonds, investors are acting contrary to the market. Since rating changes are well anticipated by market participants, sometimes relatively large shifts in index sector weightings can suddenly occur. An example of this is the energy sector. In 2014 and 2015 a number of companies in this sector lost their investment grade rating. However, the bonds were not included in the index until they were already trading at a discount to their fair value. Investors that bought at this point in time benefited from a subsequent recovery.

Actively managed funds or ETFs as an investment vehicle

Investors basically have two options for participating in fallen angel investing. Firstly, they may choose actively managed bond funds. With these, the portfolio managers are free to give preference to specific investment regions. They also seek to achieve added value over the segment average through focused selection of sectors and individual bonds.

Meanwhile, ETF solutions track an underlying index. Their main advantages include lower costs and broad diversification. For instance, the fallen angel index referred to mostly contains bonds from North America and Europe, mixed in with a smaller share of bonds from emerging market economies, with South America being one of the focal points. With global diversification, investors reduce their dependence on the economic climate in the euro area and benefit from higher levels of returns in other parts of the world. However, possible currency fluctuations need to be considered.

Conclusion

Fallen angels offer an attractive field for bond investors. Those that acquire a portfolio of these bonds today and hold it to maturity or until redemption by the issuer may achieve a structural outperformance as against the broad high yield market.

More information on the VanEck Global Fallen Angel High Yield Bond UCITS ETF

Important Disclosure

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

Related Insights

Related Insights

14 March 2024

14 March 2024